The 2026 Succession Cliff: Why Waiting for 2027 is a Risky Bet for Hospice and Home Health Owners

The M&A window for home health or hospice owners is wide open in 2026, but it will not stay that way. This post breaks down why the combination of regulatory certainty, record buyer capital, and the looming succession cliff makes this year the optimal time to explore a sale. If you are an owner generating $2M to $10M in revenue, waiting for 2027 could cost you hundreds of thousands in valuation. Here is what you need to know before the window closes.

1/29/20266 min read

This post explores why 2026 represents the optimal window for home health or hospice owners to transition their agencies. We break down the market dynamics, regulatory certainty, and buyer activity that make waiting until 2027 a gamble you may not want to take.

Quick-Scan Summary

Who this is for:

Home health or hospice agency owners generating $2M to $10M in annual revenue

Operators considering an exit within the next 12 to 24 months

Founders experiencing burnout or lacking a clear succession plan

Key takeaways:

Deal volume surged to 105 transactions in 2025, and buyer capital is stacked heading into 2026

The 2026 Medicare Final Rule provides regulatory clarity that disappears once we enter the 2027 rulemaking cycle

40% of healthcare executives will hit retirement age in the next five years, creating a "succession cliff"

Waiting for better interest rates in 2027 ignores the capital overhang available right now

Strategic buyers like Senate Healthcare are actively seeking agencies that fit their growth model

The Market Shift You Cannot Ignore

If you have been watching the home health or hospice M&A space, you already know that 2025 ended on a high note. According to Mertz Taggart's Q4 2025 Home-Based Care M&A Report, the year closed with 105 completed transactions in the home-based care sector. That is not a blip. That is momentum.

What drove this surge? A combination of interest rate cuts in late 2024 and early 2025, stabilizing Medicare reimbursement expectations, and a mountain of private equity capital that has been sitting on the sidelines since 2022.

Now, heading into 2026, that capital has not gone anywhere. In fact, it has grown. Industry analysts are calling this the "Capital Overhang" phenomenon, where strategic and financial buyers have more dry powder than quality targets to deploy it on.

For owners in the $2M to $10M revenue band, this creates a unique opportunity. Buyers are not just looking for mega-deals. They are actively pursuing well-run, mid-sized agencies that can be integrated into larger platforms. As we discussed in our piece on the 2026 dry powder surge, agencies in your revenue range are exactly what strategic acquirers are hunting for.

Regulatory Certainty: A Window That Will Not Stay Open

Here is where things get tactical. The 2026 Medicare Final Rule (CMS-1828-F) is already published. For buyers, this is gold. We know what the payment landscape looks like. We can model cash flows, forecast margins, and underwrite deals with confidence.

But 2027? That is a blank page.

Every year, CMS issues a proposed rule in the spring and a final rule in the fall. That means by mid-2026, the industry will be bracing for whatever changes are coming in 2027. New adjustments, potential cuts, behavioral assumption tweaks. The uncertainty alone causes buyers to tighten their criteria and discount offers.

For a deeper dive into how these reimbursement changes impact agency value, check out our analysis on reimbursement and regulatory updates.

The bottom line: Selling in a known regulatory environment almost always yields better multiples than selling into uncertainty.

The Succession Cliff is Real

Let's talk about the human side of this equation. According to recent healthcare leadership data, 40% of healthcare executives will reach retirement age over the next five years. Meanwhile, 58% of hospitals do not have a formal succession plan for their C-suite, and the numbers are likely worse for independent home health or hospice agencies.

If you are a founder or owner-operator, you probably did not build your agency with an exit in mind. You built it to serve patients and create something meaningful. But the reality is that burnout is real, and the industry is changing faster than ever.

Waiting until 2027 to figure out your succession plan means competing with a wave of other owners who are all hitting the same wall at the same time. More supply, same demand. That is not math that works in your favor.

We explored this dynamic in succession planning as a strategic advantage. The owners who treat their exit as a strategic move, not a last resort, consistently walk away with better outcomes.

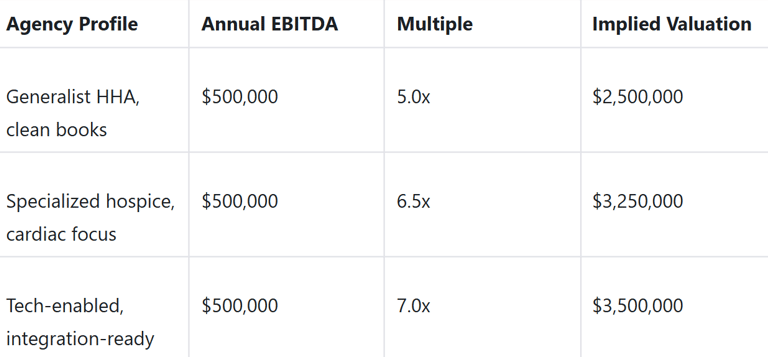

The Valuation Math: Why Timing Matters

Let's put some numbers on this. In the current market, well-run home health or hospice agencies are trading at 5x to 7x adjusted EBITDA for strategic acquisitions. Some specialized agencies are commanding even higher multiples.

Here is what that looks like in practice:

That is a $1,000,000 difference between a generalist agency and one that is positioned for a premium exit. Same EBITDA, vastly different outcomes.

Now imagine what happens to those multiples when 2027 regulatory uncertainty kicks in. Buyers get conservative. Multiples compress. That 6.5x becomes 5.5x, and your $3.25M valuation drops to $2.75M overnight.

For more on how specialization impacts your exit, read our take on why niche hospice agencies fetch higher multiples.

The "Wait for Better Rates" Myth

Some owners are holding out for 2027 because they expect further interest rate cuts. The logic sounds reasonable: lower rates mean cheaper financing for buyers, which should mean higher offers.

But here is what that logic misses: buyers already have the capital.

The capital overhang we mentioned earlier means that well-capitalized buyers are not waiting for financing. They are ready to deploy now. In fact, many strategic buyers prefer to move before rates drop further because lower rates bring more competition into the market.

Waiting for "better conditions" often means waiting yourself into a crowded field of sellers, all chasing the same pool of buyers.

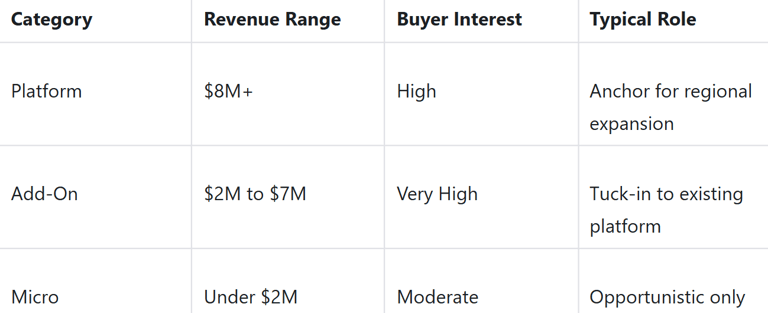

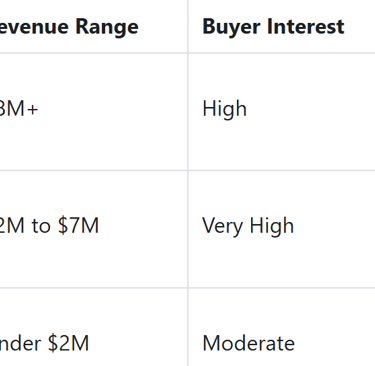

Platform vs. Add-On: Where Do You Fit?

Understanding how buyers categorize your agency helps you set realistic expectations. Here is a simple breakdown:

If your agency falls in the $2M to $10M range, you are in the sweet spot for add-on acquisitions. Strategic buyers like Senate Healthcare are specifically targeting agencies in this band because they offer immediate integration potential without the complexity of a full platform build.

So What Should You Do Now?

If you are reading this and feeling the pull to act, here are four concrete steps to take before the 2026 window closes:

Get your financials audit-ready. Clean books with normalized EBITDA are non-negotiable. Buyers will discount anything that looks murky.

Document your key processes. If the agency cannot run without you for 30 days, that is a red flag. Start building SOPs now.

Assess your clinical specialization. Do you have disease-specific programs (cardiac, neuro, pediatric)? If not, consider whether you can develop one before going to market.

Talk to a strategic buyer directly. You do not always need a broker. A direct conversation with an acquirer like Senate Healthcare can clarify your options faster than you think. We wrote about this in Do You Really Need a Broker?

Plain-Language Glossary

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. Think of it as your agency's operating profit before accounting adjustments.

Multiple: The number a buyer multiplies your EBITDA by to arrive at a purchase price. Higher multiples mean higher valuations.

Capital Overhang: When buyers have more money ready to deploy than there are quality agencies available to buy.

Add-On Acquisition: When a larger company buys a smaller agency to "add on" to an existing platform they already own.

Regulatory Certainty: When the rules (like Medicare payment rates) are known and stable, making it easier for buyers to forecast and commit.

Let's Talk About Your Next Chapter

At Senate Healthcare, we are actively pursuing home health or hospice agencies that align with our growth strategy. We are not brokers or advisors. We are operators and acquirers looking for agencies in the $2M to $10M revenue range that want a partner, not just a payout.

If you are thinking about your exit, whether that is in six months or two years, we would welcome the chance to have a direct conversation. No pressure, no pitch. Just a candid discussion about where you are, where you want to be, and whether Senate Healthcare might be the right fit.

Ready to explore your options? Schedule a consultation or visit senatehealthcare.com/about-us-home-healthcare-exit-strategy to learn more about how we approach acquisitions.

Resources:

https://www.mertztaggart.com/post/q4-2025-home-based-care-m-a-report

https://hospicenews.com/2025/12/30/the-hospice-ma-locomotive-gains-momentum-in-2025/

https://www.stoneridgepartners.com/2025/12/08/home-health-index-2025-november-update/

https://hospicenews.com/2026/01/12/5-hospice-trends-to-watch-in-2026/

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED