The 2026 "Dry Powder" Surge: Why Private Equity is Aggressively Targeting $2M–$10M Agencies Right Now

Private equity firms are sitting on over $2 trillion in unspent capital, and mid-market hospice and home health agencies are squarely in their crosshairs. This article explains why the $2M to $10M revenue range is the "sweet spot" for 2026 acquisitions and what owners can do right now to maximize their exit value. Learn the difference between platform deals and add-on acquisitions, and discover the five steps that separate prepared sellers from those who leave money on the table.

1/19/20265 min read

This post breaks down why private equity firms are sitting on record amounts of unspent capital and how that creates a unique window for hospice and home health owners in the $2M to $10M revenue range. You will learn why your agency size is the "sweet spot" for 2026 deals and what steps you can take to maximize your exit value before the window closes.

Quick-Scan Summary for Owners

Who this is for: Hospice and home health agency owners with $2M to $10M in annual revenue who are considering a sale, recapitalization, or partnership in 2026.

Key takeaways:

Private equity firms have over $2 trillion in "dry powder" (unspent committed capital) that must be deployed soon.

Agencies in the $2M to $10M range are ideal add-on acquisition targets for PE roll-up strategies.

Owners who prepare their financials and operations now can capture 0.5x to 1.5x higher EBITDA multiples.

Poor succession planning can cost you 15% to 30% of your agency's total valuation.

Q1 and Q2 2026 represent a strategic window before capital deployment cycles shift.

Applies to: Both hospice and home health agencies. While deal structures may vary slightly, the PE appetite for mid-market healthcare services is sector-wide.

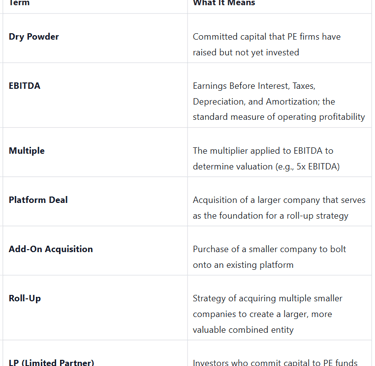

What is "Dry Powder" and Why Should You Care?

Let's start with the basics. "Dry powder" is industry jargon for the committed but unspent capital that private equity firms have raised from their investors (called Limited Partners or LPs). Think of it as money that's been promised but is sitting on the sidelines waiting for the right deals.

Here's why this matters to you: PE firms don't get to keep that money forever. They operate on fund cycles, typically 5 to 7 years, and they face pressure to deploy capital and generate returns. When dry powder piles up, firms get aggressive. They start hunting for acquisitions.

As of early 2026, estimates put global PE dry powder somewhere between $880 billion and $2.2 trillion. That's a staggering amount of capital looking for a home.

Why $2M to $10M Agencies Are the "Sweet Spot"

You might assume that PE firms only want massive healthcare systems. And yes, megafunds do chase nine and ten-figure transactions for efficiency. But here's what most owners miss: the real action for mid-market healthcare happens in roll-up strategies.

The roll-up playbook works like this:

A PE firm acquires a "platform" company (usually $10M+ in revenue with strong infrastructure).

They then bolt on smaller "add-on" acquisitions to expand geography, service lines, and patient census.

The combined entity benefits from economies of scale, centralized operations, and improved margins.

The whole package gets sold at a premium multiple a few years later.

Your $3M, $5M, or $8M agency? That's exactly what buyers need to feed the machine.

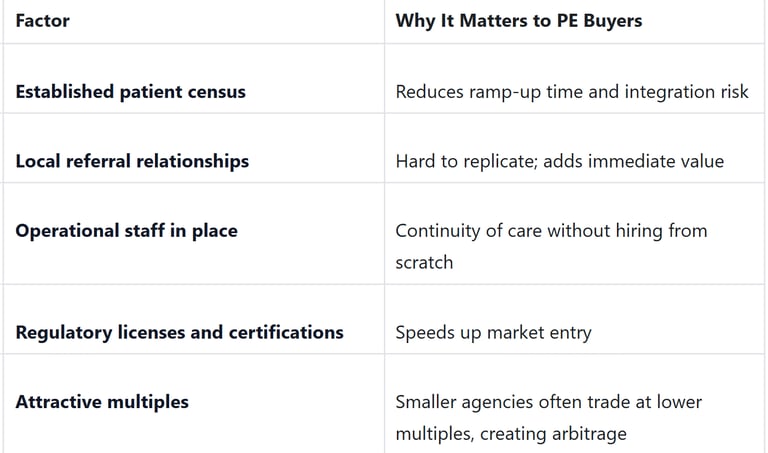

Why you're attractive as an add-on:

The bottom line: PE firms can buy your agency at a 4x to 6x EBITDA multiple, fold it into a platform, and eventually exit at 8x to 10x. Your agency is the building block that makes that math work.

The Real Numbers: What This Means for Your Exit

Let's make this concrete. Say you're a hospice owner with $4M in annual revenue and $600K in adjusted EBITDA.

Scenario A: You sell without preparation

Multiple: 4.5x EBITDA

Sale price: $2.7M

Poor documentation and succession gaps cost you 15% to 30% in valuation haircuts

Net proceeds after discounts: $1.9M to $2.3M

Scenario B: You optimize before going to market

You clean up your financials, formalize your QAPI program, and document your referral relationships

Systems improvements boost your effective multiple by 0.5x to 1.5x

Multiple: 5.5x to 6x EBITDA

Sale price: $3.3M to $3.6M

That's a difference of $1M or more in your pocket. And it often comes down to preparation, not luck.

Senate Healthcare's data shows that owners who engage in succession planning as a strategic advantage consistently outperform those who rush to market unprepared.

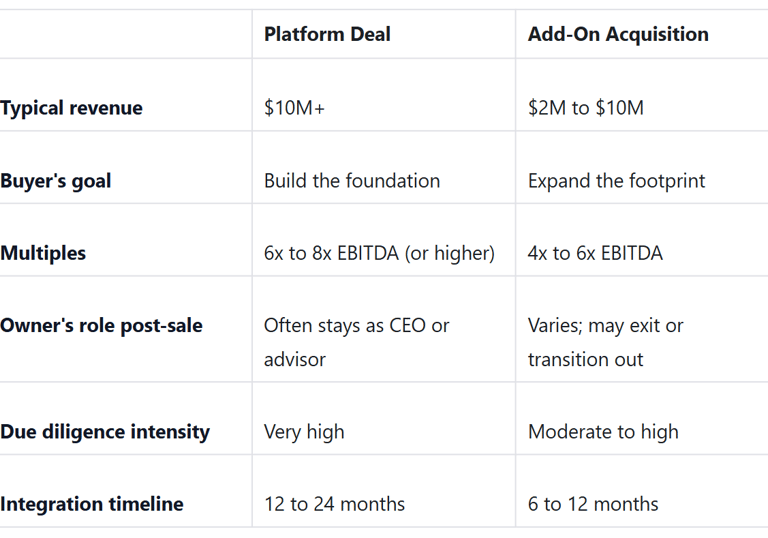

Platform Deals vs. Add-On Acquisitions: Know the Difference

Not all deals are created equal. Understanding where you fit helps you negotiate smarter.

If you're in the $2M to $10M range, you're most likely looking at an add-on scenario. That's not a bad thing. Add-on deals can close faster, involve less operational disruption, and still deliver strong returns if you're prepared.

For a deeper dive into what buyers look for in 2026 deals, check out M&A Surge Secrets Revealed: What Private Equity Buyers Don't Want You to Know.

5 Steps to Position Your Agency Before the Window Closes

The dry powder surge won't last forever. Capital deployment cycles shift, interest rates fluctuate, and buyer priorities evolve. If you're thinking about an exit in the next 12 to 24 months, here's your playbook:

1. Get your financials audit-ready

Buyers will scrutinize your revenue recognition, payor mix, and EBITDA adjustments. Clean books command higher multiples. If you haven't already, review our guide on compliance mistakes that can tank your valuation.

2. Document your referral relationships

Informal handshake deals with hospital discharge planners don't survive due diligence. Formalize agreements and demonstrate relationship continuity.

3. Strengthen your clinical leadership bench

Buyers worry about key-person risk. If your agency falls apart without you, that's a red flag. Build a leadership team that can operate independently.

4. Optimize your payor mix

Heavy Medicare Advantage exposure with declining reimbursement rates can hurt your margins. Diversify where possible.

5. Engage an advisor early

Don't wait until you have a letter of intent to bring in help. Senate Healthcare's operator-first approach focuses on maximizing your legacy and your exit value before you ever talk to buyers.

Plain-Language Glossary

The Bottom Line: Your Window is Open

Private equity's dry powder problem is your opportunity. Firms need to deploy capital, and mid-market hospice and home health agencies are exactly what roll-up strategies require.

But opportunity without preparation is just potential. The owners who win in 2026 will be the ones who clean up their operations, document their value, and engage advisors who understand healthcare M&A from the operator's perspective.

If you're considering a sale, recapitalization, or strategic partnership in the next 12 to 24 months, now is the time to start preparing.

Ready to explore your options? Schedule a healthcare partnership consultation with Senate Healthcare to discuss your exit strategy and valuation potential.

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED