Do You Really Need a Broker to Sell Your Home Health Agency? Here's the Truth

Thinking about selling your home health agency but unsure if you need a broker? This post breaks down the real differences between traditional brokers and strategic advisors, shows you how the wrong choice can cost you $500K or more, and gives you five questions to ask before signing any engagement letter. If you are a home health or hospice owner weighing your options, this is the guide you need before making a decision.

1/22/20266 min read

This post breaks down when hiring a broker makes sense for selling your home health or hospice agency and when a strategic partnership advisor might be the smarter move. We cover the real math behind representation choices and give you a framework to decide what's right for your situation.

Quick-Scan Summary

Who this is for:

Home health or hospice agency owners considering a sale in the next 12 to 36 months

Operators who have been approached by brokers or buyers and want to understand their options

Founders unsure whether professional representation is worth the commission

Key takeaways:

You are not legally required to use a broker, but going it alone rarely maximizes value

Traditional brokers and strategic advisors serve different purposes and charge differently

The wrong representation can cost you $500K or more on a mid-sized agency sale

Asking the right five questions before signing any engagement letter protects your outcome

The Real Question: Do You Need a Broker?

Let's get straight to the point. There is no law that says you must hire a broker to sell your home health agency. You can legally negotiate directly with a buyer, sign the purchase agreement yourself, and close the deal without any intermediary.

But "can" and "should" are two very different things.

The typical sale process for a healthcare agency takes 6 to 12 months and involves financial documentation, buyer outreach, due diligence, regulatory filings like Medicare Change of Ownership (CHOW) applications, and legal negotiations. Most owners have never done this before. Buyers, on the other hand, do this for a living.

That imbalance is where representation earns its keep. The real question is not whether you need help. The question is what kind of help actually moves the needle on your final sale price and deal terms.

What Traditional Brokers Actually Do (and Don't Do)

A traditional business broker or M&A intermediary handles the mechanics of bringing your agency to market. Their core services typically include:

Valuation estimates based on comparable transactions

Marketing materials like a Confidential Information Memorandum (CIM)

Buyer outreach through their network or listing platforms

Confidentiality management through blind listings and NDAs

Deal coordination between you, the buyer, attorneys, and accountants

This is valuable work. A good broker can save you dozens of hours and prevent rookie mistakes that kill deals.

However, most traditional brokers are generalists. They sell dry cleaners, dental practices, and HVAC companies using the same playbook. Healthcare agencies have unique considerations: Medicare certification, state licensure, payer mix, compliance history, and clinical staffing ratios. A generalist broker may not know how to position these factors to sophisticated healthcare buyers.

More importantly, brokers are typically compensated on a success fee basis, usually 8% to 12% of the transaction value. Their incentive is to close a deal. Your incentive is to close the right deal at the highest valuation with terms that protect your legacy and your team.

Those incentives are not always aligned.

The Hidden Cost of the Wrong Representation

Here is where the math matters.

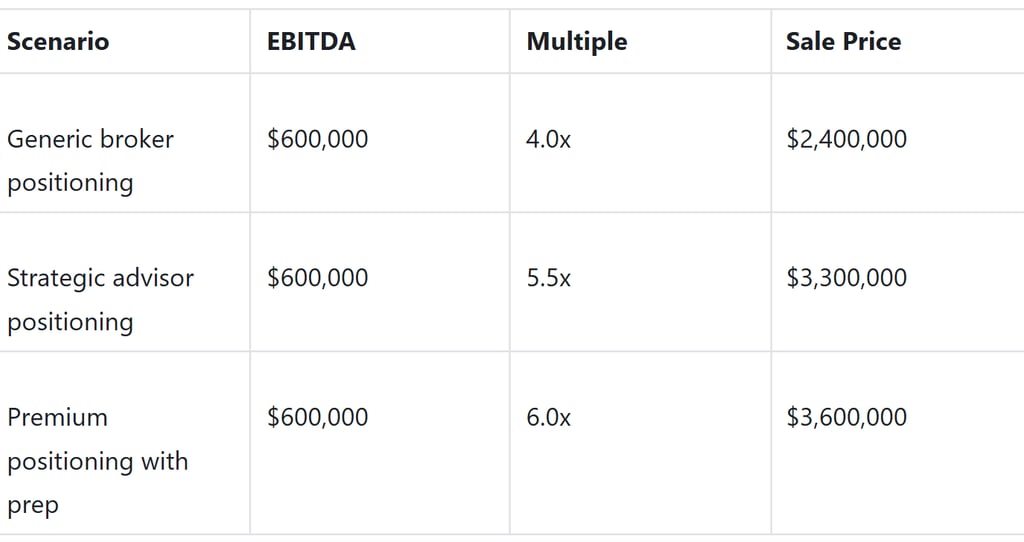

Suppose you own a home health agency generating $5 million in revenue with $600,000 in adjusted EBITDA. A broker who positions your agency as a generic small business might attract buyers offering 4x EBITDA. That gets you a $2.4 million sale price.

Now imagine a strategic advisor who understands the healthcare M&A landscape. They know that agencies with clean compliance records, diversified payer mixes, and documented succession plans command premiums. They position your agency to buyers who will pay 5.5x to 6x EBITDA. At 5.5x, your sale price jumps to $3.3 million.

That is a $900,000 difference on the same agency.

Even after paying advisory fees, the net outcome with strategic representation is dramatically higher. The difference often comes down to how the advisor positions your agency's operational strengths, not just your financials.

For example, demonstrating that you have implemented AI-driven operational improvements or a proven staff retention framework signals to buyers that your agency is not a fixer-upper. It is a turnkey asset. That perception directly impacts the multiple they are willing to pay.

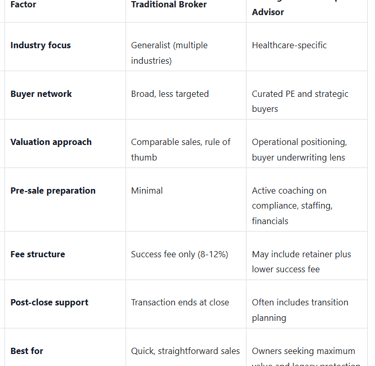

Traditional Broker vs. Strategic Partnership Advisor

Not all representation is created equal. Here is how the two main options compare:

If your primary goal is speed and simplicity, a broker may be sufficient. If your goal is maximizing valuation, protecting your team, and finding the right cultural fit with a buyer, a strategic advisor is worth the conversation.

When a Broker Makes Sense vs. When You Need More

A traditional broker may be the right fit if:

Your agency is smaller (under $1.5 million in revenue) and straightforward

You have already identified a buyer and just need transaction support

Speed matters more than squeezing out every dollar of value

You are comfortable negotiating deal terms yourself

A strategic advisor is likely the better choice if:

Your agency is in the mid-market range and attractive to PE or strategic acquirers

You want help positioning operational strengths to command premium multiples

Succession planning, staff retention, or compliance gaps need to be addressed before going to market

You want someone in your corner who understands healthcare-specific buyer concerns

The decision comes down to your goals. If you treat the sale as a transaction, hire a transactional resource. If you treat it as the culmination of years of work building something meaningful, invest in representation that reflects that.

The 5 Questions to Ask Before You Hire Anyone

Before you sign an engagement letter with any broker or advisor, ask these five questions:

How many home health or hospice agencies have you sold in the last 24 months? Look for specific experience, not general M&A credentials.

What is your buyer network in the healthcare space? A strong advisor should be able to name specific PE firms, strategic acquirers, or platforms they have relationships with.

How do you approach pre-sale preparation? If the answer is "we just list it," that is a red flag. The best outcomes come from positioning work before going to market.

What is your fee structure, and how does it align with my goals? Understand whether they are incentivized to close fast or to maximize your outcome.

What happens after the close? Transition planning, staff communication, and regulatory filings do not end at signing. Make sure your representation extends through the finish line.

The Bottom Line: Representation Matters, But the Right Representation Matters More

You do not need a broker to sell your home health agency. But you probably need someone in your corner who understands the nuances of healthcare M&A, knows how to position your agency to the right buyers, and is aligned with your goals beyond just closing a deal.

The difference between a 4x and a 6x multiple is not luck. It is preparation, positioning, and the right representation.

At Senate Healthcare, we have navigated these exact conversations many times for owners like you. We know what buyers are looking for, what red flags kill deals, and how to turn operational strengths into valuation premiums. If you are considering a sale in the next 12 to 36 months, schedule a consultation and let's talk through your options. No pressure, no pitch. Just a clear-eyed conversation about what your agency is worth and how to get there.

Plain-Language Glossary

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. A measure of your agency's operating profit that buyers use to compare businesses.

Multiple: The number buyers multiply your EBITDA by to calculate a purchase price. A 5x multiple on $600K EBITDA equals a $3 million valuation.

LOI (Letter of Intent): A non-binding document where a buyer outlines the proposed deal terms before due diligence begins.

CIM (Confidential Information Memorandum): A detailed document about your agency shared with serious buyers after they sign an NDA.

CHOW (Change of Ownership): The regulatory filing required to transfer Medicare certification from the seller to the buyer.

Success Fee: A commission paid to a broker or advisor only when the deal closes, typically a percentage of the sale price.

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED