Private Equity Is Back: Q2 2026 Deal Activity Up 18% : What Buyers Are Looking for Now

Is now the right time to sell your home health or hospice agency? With Q2 2026 deal activity up 18% and private equity buyers flooding the market, the current window for a high-value exit is wide open. We dive into the latest valuation multiples, the impact of the CMS enrollment moratorium, and the critical steps owners must take to avoid valuation haircuts during the underwriting process.

7/13/20266 min read

This post analyzes the recent surge in home health or hospice acquisition activity and provides specific valuation benchmarks for owners considering a transition. We break down the latest Q2 2026 data to help you understand how current market shifts impact your agency's sale price and exit readiness.

Quick-Scan Summary

Who this is for

Home health and hospice agency owners with $2 million to $10 million in annual revenue.

Operators feeling the pressure of regulatory shifts and considering a strategic partnership or full sale.

Healthcare entrepreneurs planning for succession within the next twelve to twenty-four months.

Key takeaways

Deal volume rose 18% in Q2 2026 with private equity backing nearly 70% of all transactions.

Valuation multiples remain strong for high-quality assets with hospice platforms reaching as high as 14x EBITDA.

A nationwide CMS enrollment moratorium is currently increasing the scarcity value of existing provider numbers.

Preparation for a Quality of Earnings (QoE) audit is now a baseline requirement for any deal exceeding $1.5 million in EBITDA.

The Q2 2026 Resurgence: Data and Dynamics

The second quarter of 2026 has marked a definitive turning point for home health or hospice M&A activity. According to the latest Hendon Partners Q2 2026 Home-Based Care M&A Report, the industry tracked between 95 and 110 transactions during this three-month window. This represents an 18% increase from the first quarter of the year. The total disclosed deal value surpassed $4.2 billion, signaling that capital is flowing back into the sector with significant momentum.

Private equity firms continue to dominate the landscape. PE-backed buyers accounted for approximately 68% of the total deal flow this quarter. These buyers are specifically looking for "platform" investments that they can use to roll up smaller agencies. This trend is particularly relevant for owners in the $2 million to $10 million revenue band. While the market is active, the scrutiny applied during underwriting has reached new heights.

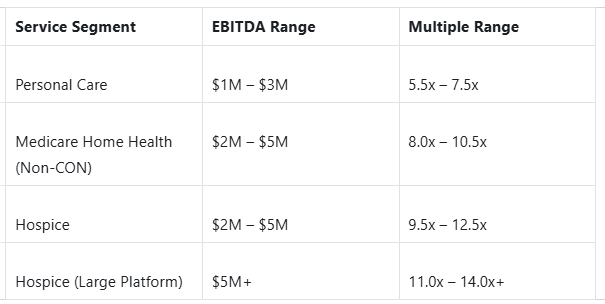

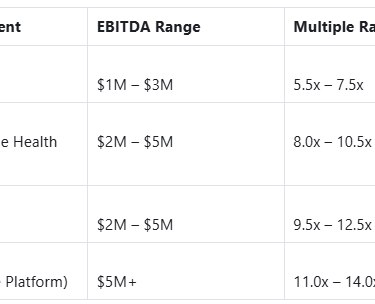

Understanding the Multiples: What is Your Agency Worth?

Valuation is rarely a single number. It is a range influenced by your specific care segment, geography, and operational health. The Stoneridge Partners May 2026 Home Health Index highlights a stable pricing environment where premium assets still command top-tier multiples.

For owners evaluating their exit strategy, these current benchmarks provide a realistic starting point for discussions:

To see how these multiples translate into a real-world sale price, consider an agency with $3 million in EBITDA. In the non-CON Medicare home health space, that agency might be valued between $24 million and $31.5 million. However, achieving the higher end of that bracket requires more than just a clean census. It requires proof of clinical quality and management depth that can survive the owner's departure. You can learn more about these drivers in our guide on moving the needle on your HHA or hospice multiplier.

The New Standard of Underwriting

In 2026, the "handshake deal" is a relic of the past. Professional buyers now require a Quality of Earnings (QoE) report for almost any transaction where EBITDA exceeds $1.5 million. This is an intensive third-party financial audit that looks past your tax returns to find the true recurring cash flow of the business.

One of the most frequent friction points we see in late-stage negotiations involves working capital disputes. Buyers are looking for a "normal" level of working capital to stay in the business at closing. If your accounts receivable are aging beyond sixty days or your billing cycle is disorganized, it can lead to significant last-minute valuation haircuts. We recommend reviewing our 10-point checklist for a 2026 audit to avoid these pitfalls.

Furthermore, the CMS 80/20 rule for Medicaid HCBS is actively shaping how buyers view personal care valuations. This rule requires that 80% of Medicaid payments go toward direct care worker compensation. Buyers are underwriting deals with the assumption that administrative margins will be squeezed, which puts a premium on agencies that have already optimized their back-office efficiency through technology.

The Enrollment Moratorium Scarcity Factor

A major driver of the current activity surge is the CMS enrollment moratorium that was announced in May 2026 and is scheduled to remain in effect through November 2026. This nationwide six-month freeze on new Medicare enrollments for home health or hospice providers has made existing provider numbers significantly more valuable.

Instead of starting new "de novo" locations, large strategic buyers and PE firms are forced to acquire existing agencies to enter new markets. This supply constraint is putting upward pressure on valuations, particularly in desirable geographic regions. For an owner, this means the current window of time represents a unique period of leverage. If you have a clean provider number and a history of compliance, you are holding a rare asset in the current market.

Culture and the Management Trap

Many owners believe their agency is worth more because they are personally involved in every patient case. From a buyer's perspective, this is a risk known as key-person dependence. If the business cannot function without you, it is much harder to sell.

Data from McKinsey indicates that companies that actively manage their organizational culture during a transition are 50% more likely to meet their synergy targets. Buyers in Q2 2026 are placing a high value on "management depth." They want to see a clinical director and an office manager who are empowered to make decisions. If you are looking to maximize your sale price, your priority should be working yourself out of the daily operations.

Real World Scenario: The $4 Million Decision

Consider Sarah, an owner of a hospice agency with $4 million in EBITDA. She was burnt out and originally planned to wait until 2028 to sell. However, after seeing the 12.5x multiples being offered in Q2 2026 and the looming November enrollment moratorium, she decided to explore a sale.

Because she had a diversified referral base and a technology-forward clinical team, she avoided the common valuation haircuts associated with concentrated referral sources. By partnering with a strategic buyer like Senate Healthcare, she was able to secure a valuation that reflected her agency's platform potential. This move effectively protected her legacy while providing her the liquidity to retire on her own terms. Owners often ask similar questions during their initial confidential consultations.

So what should you do now?

If you are an operator considering a sale or partnership, the following steps are critical for maximizing your valuation:

Request a Preliminary QoE Audit: Identify any financial or compliance red flags before you even talk to a buyer.

Evaluate Your Management Depth: Transition key responsibilities to your leadership team to reduce key-person risk.

Audit Your Payer Mix: Shift away from low-rate Medicare Advantage contracts and focus on high-quality referral relationships.

Review Your Working Capital: Clean up your accounts receivable to ensure there are no disputes during the final stages of a deal.

Plain-Language Glossary

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. This is the standard measure of a company's operating profitability.

Multiple: The number that a buyer multiplies your EBITDA by to determine the total purchase price (e.g., 8x or 10x).

Quality of Earnings (QoE): A rigorous financial review that confirms the accuracy of your financial statements and the sustainability of your profits.

Equity Rollover: A deal structure where the seller keeps a portion of their ownership in the new, combined entity rather than taking 100% cash at closing.

CON (Certificate of Need): A regulatory requirement in some states that limits the number of healthcare providers allowed to operate, often increasing the value of those that do.

Partner with Senate Healthcare

At Senate Healthcare, we are not brokers or agents. We are the buyers. We are actively evaluating home health or hospice acquisitions to expand our portfolio of high-quality care providers. Our goal is to partner with owners who have built strong agencies and are looking for a professional, confidential exit or growth partnership. We handle the complexities of the acquisition process so that you can focus on your legacy and your team.

If you are ready to explore what a sale or partnership could look like for your agency, contact us today for a confidential discussion about your exit readiness and valuation potential.

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED