10 Valuation Drivers Buyers Actually Care About: Moving the Needle on Your HHA or Hospice Multiplier in 2026

This article breaks down the 10 valuation drivers that strategic buyers like Senate Healthcare actually prioritize when underwriting home health or hospice agencies in 2026. We walk through real examples, valuation math, and the factors that can create a $4M+ swing in your exit value. If you're planning a sale or succession in the next 12 to 24 months, this is your roadmap to understanding where you stand and what levers to pull to maximize your multiplier.

2/2/20267 min read

If you're considering an exit or partnership in the next 12 to 24 months, understanding what actually moves your valuation multiplier is critical. This post breaks down the 10 drivers strategic buyers like Senate Healthcare prioritize when underwriting home health or hospice agencies, complete with examples, benchmarks, and the valuation math that shows how much each factor can impact your sale price.

Who This Is For

Home health or hospice agency owners generating $2M to $10M in annual revenue

Operators actively planning a 2026 or 2027 exit or succession event

Founders trying to understand what "premium" really means when buyers talk about multiples

Leaders who want to improve their agency's positioning before going to market

Key Takeaways

Valuation is not just about revenue. Buyers underwrite risk, reimbursement exposure, and operational scalability, which means two $5M agencies can trade at wildly different multiples.

The gap between "distressed" and "premium" can be three to four EBITDA turns, translating to millions of dollars in real exit value.

Clinical specialization, quality metrics, and staff stability are among the highest-impact levers owners can pull in the 12 to 18 months before a sale.

You don't need to be perfect to start the conversation. Strategic buyers like Senate Healthcare work with agencies at different stages of readiness.

The 2026 Valuation Landscape: Why the Multiplier Range Is So Wide

According to recent data from Mertz Taggart and Stoneridge Partners, home health or hospice agency valuations in 2026 are ranging from 2x to 10x+ EBITDA depending on risk profile, payer positioning, and operational performance. That spread is not random. It reflects how much buyers are willing to pay to acquire agencies that reduce integration risk, improve portfolio margins, and deliver predictable, recurring cash flow.

For owners in the $2M to $10M revenue band, the difference between a 4x and a 7x multiple on $800K in EBITDA is $2.4 million. Understanding which drivers move you from the low end to the high end of that range is the first step toward maximizing your exit value.

The 10 Valuation Drivers That Actually Move the Needle

1. Clinical Mix and Specialty Focus

Buyers pay premiums for agencies that specialize in complex, high-acuity service lines. Disease-specific expertise in cardiac care, pediatric palliative, neuro-focused rehabilitation, or post-acute wound management drives higher patient satisfaction, better clinical outcomes, and stronger referral relationships. Generalist agencies are harder to differentiate and face more commoditization pressure.

Why it matters: Specialized agencies command 1.5x to 2x higher multiples than generalist competitors in the same revenue tier, according to Stoneridge Partners' 2026 Home Health Index.

2. Quality Scores and Value-Based Performance

Star ratings, HHVBP scores, and CAHPS metrics are now core underwriting factors. Agencies in the top quartile for quality performance have lower regulatory risk, stronger referral flow from hospitals and health plans, and better positioning for Medicare Advantage contracts.

Why it matters: Buyers underwrite low-performing agencies at distressed multiples or walk away entirely. High performers see 1 to 2 EBITDA turns added to their baseline valuation.

3. Staff Retention and Turnover Rates

Workforce stability directly impacts operational risk. Agencies with turnover below 20% demonstrate strong culture, competitive compensation, and effective training programs. High turnover signals integration headaches, increased onboarding costs, and quality score volatility.

Why it matters: Low turnover reduces buyer integration risk and can add 0.5 to 1.0 EBITDA turns to your multiplier.

4. Geographic Density and Service Area Concentration

Dense service territories reduce drive time, improve visit efficiency, and lower per-patient costs. Agencies covering concentrated geographies with multiple payers in the same zip codes are more attractive than those spread thin across large rural areas.

Why it matters: High-density agencies have better unit economics and faster integration timelines, making them easier to scale post-acquisition.

5. Payer Mix and Medicare Advantage Positioning

Buyers prioritize agencies with diversified payer mix and proven Medicare Advantage relationships. MA plans represented over 50% of Medicare beneficiaries in 2026, and agencies positioned to serve value-based contracts have stronger long-term reimbursement visibility.

Why it matters: Agencies with 30%+ MA revenue often command 1 to 1.5 EBITDA turns above peers relying solely on traditional Medicare.

6. Referral Source Diversity and Stability

Agencies dependent on one or two hospital systems face concentration risk. Buyers look for diversified referral networks across hospitals, physician groups, ACOs, and health plans. Formal referral agreements and documented referral pipeline processes also add value.

Why it matters: Referral concentration is one of the fastest ways to get a valuation haircut. Diversified networks reduce buyer risk and improve multiplier positioning.

7. Compliance Record and Regulatory Standing

Clean survey history, no outstanding corrective action plans, and strong internal compliance infrastructure are table stakes. Buyers increasingly view compliance excellence as a premium driver, not just a pass/fail threshold.

Why it matters: Agencies with compliance issues trade at distressed multiples or require extensive hold-backs and earn-outs to mitigate buyer risk.

8. Operational Efficiency and Margin Performance

EBITDA margins above 15% to 20% signal strong operational discipline, effective cost controls, and scalable processes. Buyers underwrite margin expansion potential, and agencies already operating at benchmark efficiency levels are easier to integrate and grow.

Why it matters: Margin performance directly impacts your baseline EBITDA, which is the foundation of your valuation calculation.

9. Technology Integration and AI-Enabled Capabilities

AI-driven scheduling, revenue cycle automation, and predictive analytics are no longer supplementary. They are core determinants of valuation in 2026. Buyers prioritize agencies with technology stacks that enhance workforce capacity, reduce administrative burden, and improve billing accuracy.

Why it matters: Technology-enabled agencies demonstrate lower operational risk and faster scalability, adding 0.5 to 1.0 EBITDA turns in competitive processes.

10. Leadership Depth and Key-Person Risk

Agencies overly reliant on the founder for operations, referral relationships, or clinical oversight are viewed as high-risk. Buyers look for documented SOPs, cross-trained leadership teams, and operational continuity plans that reduce transition friction.

Why it matters: High key-person risk can result in earn-out structures, reduced upfront cash, or valuation discounts of 20% to 30%.

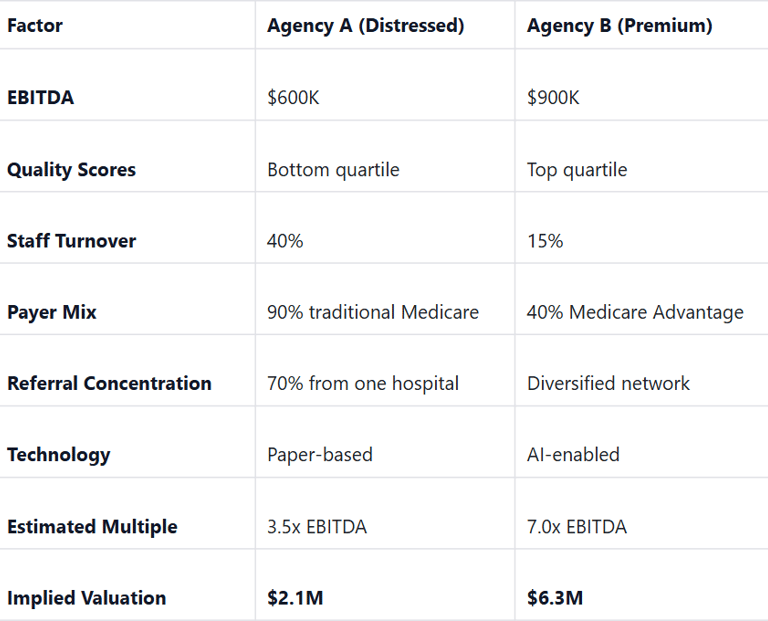

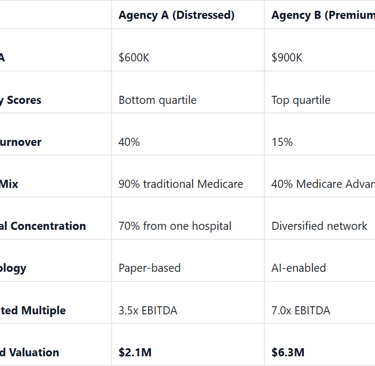

The Valuation Math: How These Drivers Translate to Real Dollars

Let's look at two hypothetical $5M home health agencies with identical revenue but very different risk profiles.

The difference? $4.2 million. Same revenue. Radically different outcomes. That gap is driven entirely by the 10 factors outlined above.

A Real-World Vignette: The Founder Who Left Money on the Table

Maria founded her hospice agency in 2011 and grew it to $6M in annual revenue by 2025. She had strong clinical outcomes, loyal staff, and a reputation in her market. But when she started exploring a sale, she discovered three problems:

Key-person risk: She was the primary relationship holder for 60% of her referral sources.

Compliance gaps: Two minor survey findings from 2024 had not been fully remediated.

Technology debt: Her agency still used spreadsheets for scheduling and manual billing processes.

Her initial offers came in at 4.0x to 4.5x EBITDA. After working with a strategic buyer to address leadership documentation, compliance remediation, and technology infrastructure over six months, she re-entered the market and closed at 6.5x EBITDA. The difference? $1.8 million in incremental exit value.

You Don't Need to Be Perfect to Start the Conversation

If your agency doesn't check every box on this list, that's normal. Most agencies in the $2M to $10M range have one or two areas that need work before going to market. The key is knowing where you stand, understanding which levers to pull, and having a realistic timeline to improve positioning before you engage buyers.

Senate Healthcare works with owners at different stages of readiness. Whether you're 24 months out or actively exploring a sale in 2026, we're interested in understanding your agency's unique strengths and challenges. Strategic buyers like us can help you identify the highest-impact improvements and structure partnerships that align with your goals, even if you're not "perfectly" positioned today.

So What Should You Do Now?

If you're serious about maximizing your exit value, here are four concrete steps to take in the next 90 days:

Benchmark your quality metrics. Pull your latest HHVBP scores, Star ratings, or CAHPS results and compare them to CMS national averages. If you're below the 50th percentile, you have valuation risk.

Audit your key-person exposure. List every critical relationship, operational process, and decision point that depends on you personally. Start documenting SOPs and cross-training leadership.

Review your payer and referral mix. Calculate how much of your revenue comes from your top three payers and top three referral sources. If it's over 60%, you have concentration risk that will impact your multiple.

Talk to a strategic buyer. Even if you're not ready to sell tomorrow, understanding how buyers underwrite your agency today gives you a roadmap for the next 12 to 18 months. Reach out to Senate Healthcare to start that conversation.

Final Thoughts: The Valuation Game Is Won Before You Go to Market

The agencies that command premium multiples in 2026 are not lucky. They are disciplined, strategic, and intentional about the drivers that matter most to buyers. Whether you're planning an exit in 2026 or positioning for 2027, the time to address quality, compliance, technology, and key-person risk is now, not six weeks before you sign an LOI.

Senate Healthcare is actively acquiring home health or hospice agencies in the $2M to $10M revenue range. If you want to explore what a strategic partnership could look like for your agency, or if you just want an honest assessment of where you stand today, let's talk.

Glossary: Key M&A Terms in Plain Language

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): A proxy for operating cash flow. Buyers use EBITDA as the baseline number to apply valuation multiples.

Valuation Multiple: The factor applied to EBITDA to determine enterprise value. A 6x multiple on $1M in EBITDA equals a $6M valuation.

Key-Person Risk: The degree to which an agency's performance depends on the founder or a single leader. High key-person risk reduces valuation.

Payer Mix: The distribution of revenue across Medicare, Medicaid, Medicare Advantage, and commercial payers. Diversified payer mix reduces reimbursement risk.

Referral Concentration: The percentage of total admissions or revenue coming from a small number of referral sources. High concentration increases buyer risk.

Value-Based Performance (VBP): CMS programs that tie Medicare reimbursement to quality metrics and patient outcomes. Strong VBP performance improves valuation.

Medicare Advantage (MA): Private health plans that contract with CMS to provide Medicare benefits. Agencies with MA relationships often command higher multiples.

Earn-Out: A deal structure where part of the purchase price is contingent on the agency hitting post-close performance targets. Often used when buyers perceive execution risk.

Resources:

https://www.mertztaggart.com/post/q4-2025-home-based-care-m-a-report

https://www.stoneridgepartners.com/2026/01/14/2026-healthcare-ma-forecast-private-equity/

https://hospicenews.com/2026/01/08/the-pendulum-swings-hospices-2026-ma-outlook/

https://www.stoneridgepartners.com/2025/12/18/home-health-agency-valuation-year-end-checklist-2026/

https://www.scoperesearch.co/post/hospice-valuation-multiples-and-m-a-trends-2025

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED