The Hidden Lever: Why Payer Mix Diversification is the Key to Your 2026 Exit Strategy

Is your agency’s valuation being held back by your revenue sources? This guide breaks down why payer mix is the most critical lever for owners planning a 2026 exit, including how to secure a "1.5 EBITDA Turn" bonus. Learn how to avoid the "60% trap" and why Senate Healthcare prioritizes agencies with strong Medicare Advantage and private-pay balances.

6/9/20266 min read

This article explores how the composition of your agency’s revenue directly dictates the multiple a buyer will pay during a sale or partnership. We examine why home health and hospice owners must shift their focus from top-line revenue to a diversified payer mix to maximize their exit valuation in the 2026 market.

Quick-Scan Summary

Who this is for:

Owner-operators of home health or hospice agencies with $2M to $10M in annual revenue.

Founders considering an exit or succession plan within the next 12 to 24 months.

Executives looking to understand how Medicare Advantage and private-pay impact their company’s market value.

Key takeaways:

Payer diversification acts as a valuation "multiplier," potentially adding 1.5x to your EBITDA multiple.

Over-reliance on a single payer (the "60% trap") creates significant underwriting risk for buyers like Senate Healthcare.

High clinical quality scores (4+ stars) are now a prerequisite for "Preferred Provider" status and premium pricing.

Private-pay revenue is increasingly valued for its fast cash conversion and lower regulatory burden.

The 2026 Market Context: From Growth at All Costs to Quality Cash Flow

The landscape for home health and hospice acquisitions has shifted dramatically. In previous years, many buyers were focused on rapid geographic expansion and sheer patient volume. Today, the focus has pivoted toward the durability and predictability of cash flow. In 2026, the primary question we ask when evaluating an acquisition is not just "How much money do you make?" but "Where does that money come from, and how hard is it to keep?"

Macroeconomic pressures, including labor costs and changing reimbursement rates, have made buyers more selective. We are looking for agencies that have insulated themselves against regulatory shifts by building a balanced revenue portfolio. If your agency is 95% dependent on traditional Medicare Fee-for-Service (FFS), you are vulnerable to the stroke of a legislative pen. Diversification is the shield that protects your valuation.

Owner Pain Points: The Hidden Risks in Your Census

Many owners we speak with at Senate Healthcare are facing a common set of challenges that threaten their exit price:

Succession Risk: Without a diversified referral and payer base, the business often relies too heavily on the owner’s personal relationships.

Buyer Underwriting Scrutiny: We look deep into the "quality of earnings." If a single Medicare Advantage contract accounts for half your volume, a rate cut or contract termination could collapse your EBITDA overnight.

Key-Person Dependence: When an agency is small, the owner is often the primary marketer. If the payers and referral sources do not have institutionalized contracts with the agency itself, the value walks out the door when the owner leaves.

Valuation Haircuts: Owners are often surprised to find that while their revenue is growing, their valuation multiple is shrinking because their "Payer Mix" is seen as high-risk.

The Valuation Math: Quantifying the Diversification Premium

Let’s look at a concrete example of how payer mix changes the literal check size at closing. Consider two home health agencies, both generating $1,000,000 in annual EBITDA.

Agency A (Concentrated Mix):

90% Medicare Fee-for-Service (FFS).

10% Low-rate Medicare Advantage.

Result: This agency is seen as a "standard" asset. In the current market, it might command a 7.0x multiple.

Valuation: $7,000,000.

Agency B (Diversified Mix):

60% Medicare Fee-for-Service (FFS).

25% High-star Medicare Advantage (Preferred Provider status).

15% Private-pay or Commercial Insurance.

Result: This agency has lower regulatory risk and proven "stickiness" with managed care. It qualifies for a 1.5 EBITDA Turn bonus.

Valuation: $8.5x multiple = $8,500,000.

By simply shifting the mix and proving the stability of those non-FFS relationships, the owner of Agency B earns an extra $1,500,000 at the sale table for the exact same bottom-line profit. This is why we refer to payer mix as the "hidden lever" of valuation.

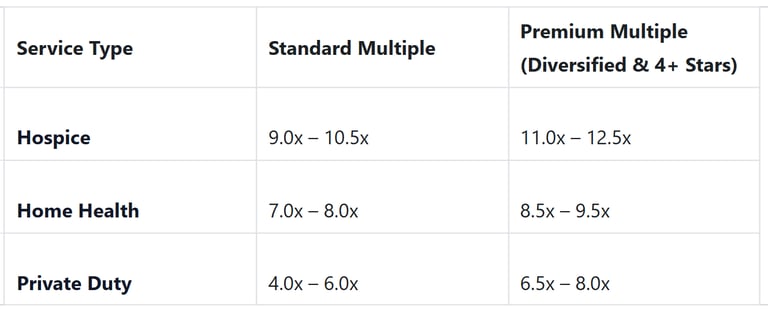

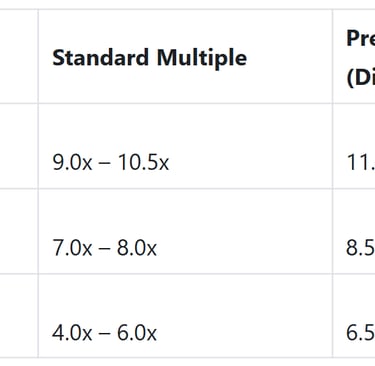

Market Benchmarks: 2026 Valuation Multiples

When you partner with or sell to an entity like Senate Healthcare, your agency is categorized based on its size, clinical performance, and payer mix. Below are the current ranges for agencies in the $2M to $10M revenue band.

Note: Multiples are applied to TTM (Trailing Twelve Months) Adjusted EBITDA.

Medicare Advantage: The 4-Star Threshold

In 2026, Medicare Advantage (MA) is no longer a "necessary evil." It is a strategic asset if managed correctly. However, not all MA revenue is created equal. We look for agencies that have achieved "Preferred Provider" status.

To reach this level, an agency typically needs a 4-star rating or higher. This rating allows you to negotiate better rates and, more importantly, reduces the administrative burden of authorizations. When we evaluate an acquisition, we look for a "4-star premium." If your agency is consistently performing at 4.5 or 5 stars, we know your MA revenue is higher-margin and lower-risk, which justifies a higher purchase price.

Avoiding the "60% Trap"

Concentration risk is the silent killer of deals. If any single payer or referral source accounts for more than 60% of your business, you have a concentration problem. From a buyer’s perspective, this represents a single point of failure. If that hospital system decides to start its own agency, or if that specific MA plan changes its network, your business could lose the majority of its value overnight.

As we look to acquire agencies at Senate Healthcare, we prefer to see a "spread" of at least 4 to 5 major referral sources and a mix of at least 3 distinct payer types.

The Private-Pay Advantage

While home health or hospice care is primarily government-funded, adding a private-pay component (often through companion care or private-duty nursing) can significantly de-risk your exit. Private-pay revenue is highly attractive to buyers because it offers:

Immediate Cash Flow: No waiting for government billing cycles or RAP (Request for Anticipated Payment) adjustments.

Lower Compliance Risk: Private contracts are not subject to the same grueling ADRs (Additional Documentation Requests) as Medicare.

Market Flexibility: You set your own rates based on local demand rather than federal mandates.

Even if private-pay only makes up 15% of your total revenue, it provides a "valuation floor" that makes your agency much more resilient during underwriting.

Plain-Language Glossary

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. Essentially, a measure of your agency's cash flow.

Multiple: The number multiplied by your EBITDA to determine the total sale price (e.g., $1M EBITDA at a 8x multiple = $8M sale).

Payer Mix: The percentage breakdown of where your money comes from (Medicare FFS, Medicare Advantage, Private Pay, Medicaid, etc.).

TTM: Trailing Twelve Months. Buyers look at your most recent 12 months of financial performance to set a price.

Concentration Risk: The danger of having too much revenue tied to one source.

So what should you do now?

If you are planning to sell your agency or explore a partnership in the next year, you should take these steps today to prepare for buyer scrutiny:

Audit Your Payer Mix: Run a report for the last 12 months. If any single payer is over 60%, begin focusing your marketing efforts on diversifying your referral base immediately.

Review Your MA Contracts: Identify which Medicare Advantage plans are your most profitable. Focus on clinical outcomes for those specific plans to secure "Preferred" status.

Monitor Your Star Rating: Clinical quality is no longer just about patient care: it is a financial metric. Moving from a 3.5 to a 4.0 star rating can directly increase your sale price.

Clean Up Your Documentation: Buyers will look for "leaky" revenue. Ensure your charts can stand up to an audit before you start the sale process.

Explore an Exit with Senate Healthcare

Senate Healthcare is actively seeking to acquire and partner with high-quality home health or hospice agencies. We are not brokers or advisors: we are a strategic buyer looking to build a national brand through operational excellence. If you have built a strong agency and are looking for a confidential consultation to explore a sale or succession plan, we are ready to talk. Our goal is to help owners maximize the value of their legacy while ensuring their patients continue to receive top-tier care.

Contact Senate Healthcare today to discuss how your agency fits into our current acquisition strategy.

Resources:

https://www.mertztaggart.com/post/q1-2026-home-based-care-m-a-report (Source for 2026 M&A volume and hospice activity)

https://www.jdsupra.com/legalnews/home-health-hospice-m-a-in-2026-why-the-1381791/ (Source for 2026 market reset and buyer discipline)

https://www.jdsupra.com/legalnews/home-health-hospice-m-a-in-2026-how-5810859/ (Source for compliance, documentation integrity, and valuation impact)

https://senatehealthcare.com/2026-home-care-manda-secrets-what-agency-owners-need-to-know-now (Related Senate Healthcare post)

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED