The "Hidden" Cost of Delay: Why Waiting for a 2027 Exit Might Cost You 15% in Valuation Based on Current M&A Headwinds

Waiting until 2027 to sell your home health or hospice agency could cost you 15% or more in valuation, erasing years of operational gains. This post breaks down why 2026's unique convergence of stable CMS rates, strong buyer appetite, and favorable financing creates a seller's market that won't last. Learn what happens to deal multiples when market conditions shift and why starting the conversation now protects your exit value.

2/19/20267 min read

If you're a home health or hospice owner thinking about waiting until 2027 to explore an exit, that delay could quietly erase hundreds of thousands of dollars in sale price. This post explains why 2026 offers a unique convergence of favorable market conditions and what happens to valuations when those conditions shift.

Quick-Scan Summary

Who this is for:

Home health or hospice owners generating $2M–$10M in annual revenue

Operators considering an exit within the next 12–24 months

Founders concerned about timing their sale during uncertain economic cycles

Leaders who want to understand how market windows impact deal multiples

Key takeaways:

2026 presents a "Goldilocks" window with stable CMS rates, manageable borrowing costs, and strong buyer appetite

Waiting for 2027 introduces federal policy uncertainty, potential reimbursement resets, and increased market saturation

A 15% drop in valuation multiple can eliminate years of operational gains and cost hundreds of thousands in sale proceeds

We structure deals that reward future growth post-acquisition, so you don't need perfect EBITDA timing to start the conversation

Why 2026 Is the Goldilocks Window

The M&A market for home health and hospice agencies doesn't move in predictable cycles. It responds to the intersection of federal reimbursement policy, interest rate environments, buyer capital availability, and operator sentiment. Right now, those forces are aligned in a way we haven't seen in years.

Here's what makes 2026 unique:

CMS finalized the FY 2026 hospice payment rule with a 2.6% rate increase, providing operators with rare reimbursement clarity and margin stability. Home health agencies benefit from similar regulatory predictability entering this year. That stability translates directly into buyer confidence. When we evaluate your agency, we can underwrite future cash flows with more precision, which supports higher purchase price offers.

Corporate borrowing costs remain broadly stable compared to the 2022–2023 spike. That means buyers like us can deploy capital efficiently without the valuation haircuts that come with elevated financing risk. Private equity firms, which drive significant deal volume in this sector, are under pressure to exit long-held positions. Average hold times increased to 6.2 years in 2025, creating urgency among funds to transact now rather than later.

Global M&A rebounded to $4.4 trillion in 2025, and U.S. deal volume reached approximately $2.3 trillion, up 49% from 2024. Strategic buyers are deploying freshly allocated capital in Q1 2026, and sellers who move now capture premium valuations before heightened competition compresses both timelines and multiples later in the year.

In short, 2026 offers the regulatory clarity, capital availability, and buyer urgency that define a seller's market. But that window won't stay open indefinitely.

John's Story: The Cost of Waiting

John ran a well-regarded hospice agency in the Southeast. His 2023 EBITDA was $1.8 million, and he had begun exploring a sale when he heard whispers that CMS might adjust hospice rates favorably in 2024. His accountant suggested he wait another 12 months to let his margins expand and "maximize the multiple."

So John waited. And while he waited, two things happened that he didn't anticipate.

First, CMS delayed the rate clarity he expected. Instead of a clean increase, the agency faced administrative scrutiny around documentation standards that compressed reimbursement timelines and created cash flow volatility. His EBITDA didn't grow. It flatlined.

Second, the buyer pool shifted. By late 2024, three competing hospice agencies in his region had already been acquired by larger platforms. Those platforms were now focused on operational integration, not new acquisitions. The strategic urgency that had driven premium offers 12 months earlier evaporated. When John finally brought his agency back to market in early 2025, the best offer he received was $800,000 lower than the letter of intent he had turned down in 2023.

John's experience illustrates what we call "market fatigue." Buyers don't wait for sellers to decide. We move capital where opportunity exists today. Delaying an exit doesn't just postpone a transaction. It changes the transaction itself, often unfavorably.

The Math on a 15% Valuation Drop

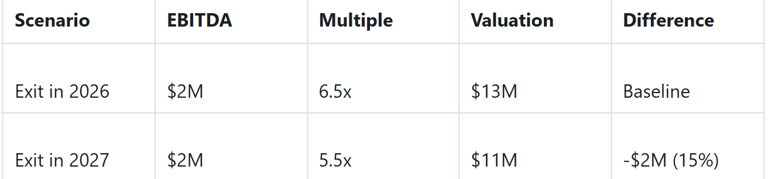

Let's make this concrete. Assume your home health or hospice agency generates $2 million in annual EBITDA. In today's market, we might offer a valuation multiple of 6.5x EBITDA for a well-run agency with strong referral networks, clean compliance, and solid retention metrics. That puts your purchase price at $13 million.

Now assume you wait until 2027, and the multiple compresses to 5.5x due to increased market saturation, regulatory uncertainty, or broader economic headwinds. Your purchase price drops to $11 million. That's a $2 million reduction, or roughly 15% of your sale proceeds, without any operational decline on your part.

Here's the breakdown:

For many owners, that $2 million represents years of reinvested profit, deferred compensation, and personal risk. Waiting doesn't just delay liquidity. It actively erodes the return you've earned.

What Changes Between Now and 2027?

The risks to valuation multiples in 2027 fall into three categories: federal policy uncertainty, reimbursement resets, and market saturation.

Federal policy uncertainty: Presidential and Congressional elections in 2024 set the stage for potential Medicare and Medicaid policy shifts taking effect in late 2026 and throughout 2027. Historically, policy transitions create buyer hesitation. When we can't confidently model reimbursement scenarios three years forward, we reduce the multiples we're willing to pay today. December 2025 saw a deal surge as strategic buyers rushed to close transactions before potential 2026 DOJ remedy changes and FTC scrutiny around vertical integrations. Those concerns haven't disappeared. They've been deferred.

Reimbursement resets: CMS rarely delivers consecutive years of favorable rate adjustments. The 2.6% increase for hospice in 2026 reflects budget reconciliation and cost-of-living factors that may not repeat in 2027. Home health rates face similar cyclicality. If 2027 brings flat or reduced reimbursement, agencies will see margin compression, and buyers will recalibrate valuations downward to reflect diminished cash flow expectations.

Market saturation: Consolidation in home health and hospice continues to accelerate. Larger platforms are expanding their geographic footprint aggressively, and once a region reaches a certain threshold of market concentration, buyer appetite for incremental add-ons declines. If your agency operates in a market where three or four competitors have already been acquired by 2027, our acquisition criteria may shift toward platform-scale opportunities rather than bolt-ons, reducing the premium we can justify for your business.

None of these risks are hypothetical. They're structural realities embedded in healthcare M&A cycles. Owners who time their exit during favorable windows capture the upside. Owners who delay often discover that the market moved on without them.

You Don't Need Perfect EBITDA to Start the Conversation

If you're concerned that your current EBITDA isn't "peak" yet, don't let that stop you from starting the conversation. We often structure deals that reward future growth post-acquisition, allowing you to capture today's high multiples while still benefiting from your agency's upward trajectory.

These structures might include earnouts tied to revenue milestones, equity rollovers that let you participate in the combined entity's growth, or performance-based compensation that aligns your incentives with ours during the transition period. The key is initiating dialogue now, while market conditions favor sellers, rather than waiting for an arbitrary operational benchmark that may never arrive or may arrive too late to matter.

We're evaluating agencies across the home health and hospice spectrum. If you're generating consistent cash flow, maintaining strong referral relationships, and operating with clean compliance, you're likely more attractive to us than you realize.

So What Should You Do Now?

Request a preliminary valuation conversation. We can provide a confidential assessment of where your agency sits in the current market without requiring you to commit to a formal sale process. Understanding your baseline valuation today gives you a reference point for decision-making.

Document your key operational metrics. Buyers like us move quickly when we see clean data. Make sure your EBITDA calculations, referral pipelines, payer mix, and compliance records are audit-ready. Agencies that can provide this visibility during initial diligence receive faster offers and smoother closings.

Map your succession timeline. If you're planning to exit within the next 18–24 months, now is the time to align operational priorities with buyer expectations. That might mean tightening staffing retention, upgrading your billing software, or formalizing referral agreements. Small improvements in these areas can meaningfully shift the multiple we apply during underwriting.

Don't wait for "perfect" conditions. Market timing is more art than science, but the data today clearly favors action over delay. The window we're describing won't close overnight, but it also won't stay open indefinitely. Owners who engage early position themselves to negotiate from strength rather than necessity.

Let's Talk About Your Exit Strategy

Senate Healthcare is actively acquiring home health and hospice agencies that align with our criteria for sustainable growth and patient-centered care. We're not brokers or advisors. We're the buyer at the table, and we structure transactions that recognize the value you've built while setting your agency up for long-term success under our platform.

If the scenarios in this post resonate with your situation, we'd like to hear from you. Reach out to us at senatehealthcare.com to explore what a 2026 exit could look like for your agency. The conversation is confidential, and there's no obligation to move forward unless the terms make sense for you.

Resources:

https://www.lazard.com/media/vnajb4v3/2025-ma-review-and-2026-outlook-report.pdf

https://privateequityinfo.com/blog/private-equity-holding-periods-continue-to-climb

https://homehealthcarenews.com/2026/02/inside-the-trends-shaping-at-home-care-ma-in-2026/

https://www.mertztaggart.com/post/the-fog-is-lifting-why-hospice-m-a-is-racing-back-in-2026

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED