The Scarcity Value of Your Provider Number: Navigating the 2026 CMS Moratorium

The 2026 CMS moratorium has effectively frozen the supply of new home health and hospice licenses, creating a high-value "scarcity premium" for existing agencies. This article explores how owners can leverage their "clean" provider numbers to secure higher EBITDA multiples and navigate the complexities of buyer underwriting in a restricted market. Learn why mid-2026 is a critical window for those considering a strategic sale or succession plan.

6/22/202611 min read

On May 13, 2026, CMS sent a shockwave through home health or hospice with a nationwide enrollment moratorium that immediately changed how owners, buyers, and operators viewed agency value. What had once been a difficult licensing environment became a true supply freeze, and that shift matters for owners thinking about succession, sale timing, valuation, and buyer scrutiny.

Quick-Scan Summary

Who this is for

Owners and operators of home health or hospice agencies in the $2M to $10M revenue range

Founders thinking about a sale, partnership, or succession plan during a high-scrutiny regulatory period

Agencies with a clean provider number, stable billing, and questions about how the moratorium affects valuation

Teams trying to understand what buyers will underwrite more aggressively in 2026

Key takeaways

The May 13, 2026 moratorium is historically significant because it applies nationwide, not just to selected metro areas or supplier categories.

Existing agencies with clean enrollment histories may now command stronger attention because new Medicare entry is frozen.

Buyers are competing for a finite pool of acquisition targets, but diligence standards are also getting tougher.

Owners who clean up billing, understand payer mix, and benchmark real EBITDA are in a stronger position to protect deal value.

The opening weeks after the announcement felt different from prior compliance headlines because this was not another regional tightening or a narrow DMEPOS action. It was a nationwide move affecting new Medicare enrollments for home health agencies and hospice providers, which immediately reframed how scarce a functioning, compliant provider number had become. For owners who remember prior moratoria tied to select counties, ZIP codes, or supplier segments, this was a bigger moment. It changed the conversation from growth planning to access, scarcity, underwriting risk, and exit timing.

That historical context matters. Previous moratoria often created local bottlenecks, but operators could still look outside the affected geography or pursue other pathways. A nationwide freeze is different because it compresses the future supply of newly enrolled agencies across the entire country at the same time. For owner-operators, especially those dealing with burnout, succession pressure, or rising compliance burden, the result is a more valuable asset on paper but also a more heavily inspected one in practice.

Plain-Language Glossary

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization. This is a common measure of a company's operating performance and a starting point for valuation.

Moratorium: A temporary prohibition or freeze on an activity. In this case, it is a freeze on new Medicare provider enrollments.

Diligence: The process a buyer uses to verify the financial and clinical health of an agency before completing a sale.

Multiples: A number used to multiply a company's EBITDA to determine its total enterprise value (for example, a 6x multiple on $1M EBITDA equals a $6M valuation).

Provider Number: The unique identifier (PTAN or NPI) that allows an agency to bill Medicare and other payers for services.

What the Freeze Actually Covers (and What It Doesn't)

The most important point for owners is this: the moratorium is not a generic industry slowdown. It is a specific Medicare enrollment freeze with very practical mechanics that affect how scarcity shows up in the market.

Based on CMS moratoria guidance and the 2026 FAQ framework cited below, the freeze blocks initial enrollments for new Medicare home health and hospice providers. In plain language, if a would-be operator does not already have an enrolled provider in place, they cannot simply file a new application and expect to enter Medicare the normal way during the moratorium period.

It also reaches beyond brand-new agencies. The freeze applies to new practice locations, branches, or expansion sites in circumstances where enrollment action would be required. That matters because some groups that planned to grow by opening satellite locations now have fewer options. Instead of building from scratch, many are forced to look at acquisition targets that are already enrolled and operational.

Owners should also understand the CIMO concept clearly. In this context, CIMO refers to a Change in Majority Ownership event. A clean provider number does not become a free pass just because a buyer wants to acquire it. Ownership transactions can trigger additional CMS review, revalidation steps, disclosure requirements, and downstream scrutiny depending on deal structure, effective dates, and state level licensing overlays. In other words, a moratorium makes existing agencies more valuable, but it does not eliminate enrollment-related risk when control changes hands.

Just as important are the exceptions. The moratorium does not mean every PECOS action is frozen. CMS has carved out several important categories that owners should know:

Change of address updates may still be processed when they are permitted under CMS rules.

Basic information updates such as phone number corrections, correspondence information, or certain administrative changes are generally not treated the same as a new enrollment.

Applications already pending before May 13, 2026 may continue through review rather than being automatically voided, depending on status and completeness.

Other case-specific exceptions may apply where CMS expressly allows them.

The timing rule matters too. Moratoria are commonly imposed for an initial six-month period, and CMS can extend them in six-month increments. That extension power is a major reason buyers are reacting now instead of waiting. If the market believes the freeze could persist beyond the initial period, then the value of already enrolled agencies may hold up longer than many operators first assumed.

For an owner in home health or hospice, the takeaway is simple: if you already have an operating agency with a clean Medicare pathway, you control something that new entrants cannot easily recreate in the short term.

Why Your Clean Provider Number Is Suddenly Worth a Premium

This is basic supply and demand, but with much bigger consequences because Medicare access is the core gatekeeper asset.

Before the moratorium, a buyer could compare two broad paths: build versus buy. Building was slow, expensive, and operationally painful, but it was still theoretically available. On May 13, 2026, that math changed. If a buyer wants exposure to home health or hospice Medicare revenue now, the number of available pathways shrinks. In many cases, acquisition becomes the only realistic route.

That creates a finite target pool. There are only so many agencies with active provider numbers, acceptable compliance history, stable census, and ownership willing to transact. Once that pool tightens, leverage begins to move toward sellers, especially sellers with records that hold up under underwriting.

Several buyer groups may now be looking at the same agency:

Private equity-backed platforms trying to secure scale in a supply-constrained market

Strategic roll-ups seeking geographic density or adjacency

Regional operators that want growth but cannot rely on de novo enrollment

New entrants who had planned to get their own licenses and now need an acquisition path instead

That does not mean every agency gets a premium. A provider number is more valuable when it is paired with clean books, coherent billing, stable leadership, and a believable transition plan. Buyers are not paying more just because a license exists. They are paying more for a license that can survive scrutiny and continue operating without post-close disruption.

Here is a simple valuation scenario to show the difference:

That spread is $1.575 million on the same EBITDA base. The moratorium can support stronger multiples for the right asset, but weak documentation or underwriting risk can still erase that upside quickly.

For hospice owners, the same logic applies even if local demand patterns and census models differ from home health. Buyers still want continuity, compliance, and reimbursement durability. For home health owners, payer diversification and PDGM execution may carry added weight. Different operating models, same core lesson: a clean provider number is now part of a scarcity story, and scarcity can improve leverage when the asset is truly financeable.

Succession Risk and the "Key-Person" Trap

Many owners in the $2M to $10M revenue bracket face a significant "key-person" risk. If the business cannot run without the owner’s daily involvement, the valuation takes a haircut during buyer underwriting. The 2026 moratorium makes this risk even more acute.

If an owner experiences burnout or health issues during a moratorium, they cannot simply assume the business will remain stable while they step back. Buyers will ask whether referral relationships, staff retention, compliance oversight, and payer communication all depend on one person. If the answer is yes, the agency may still be attractive, but the buyer will price in transition risk.

Consider two anonymized examples:

Owner A, home health: $4.5M in revenue, strong census, but the owner personally approves key billing workflows, manages referral sources, and handles all compliance escalations. Buyers see concentration risk and may lower the multiple until a management layer is installed.

Owner B, hospice: $3.2M in revenue, lean team, good local reputation, but no documented succession plan and no second-in-command. Even with decent margins, buyer underwriting may flag execution risk if the owner wants a fast exit.

If the business cannot run without the founder, valuation gets hit. During a moratorium, that hit can feel more frustrating because the provider number itself may be worth more while the operating model still drags the deal down. By partnering with an acquirer like Senate Healthcare LLC, you can transition your agency into a larger platform structure built to reduce key-person dependence, preserve continuity of care, and protect your legacy.

The Diligence Bar Has Never Been Higher

Scarcity does not reduce risk review. It raises it.

During a moratorium, regulators and buyers both become more alert to problem assets entering the market. CMS has emphasized program integrity tools, data analytics, and targeted oversight in higher-risk environments. The 2026 framework has also drawn more attention to the Provider Enrollment, Oversight, and screening focus in PPEO-targeted states, including Arizona, California, Nevada, Texas, Georgia, and Ohio. If your agency operates in or around these states, expect buyers to ask more questions, not fewer.

The payment suspension environment adds to that pressure. Reports tied to current enforcement activity have highlighted roughly $70 million in suspended payments, a useful signal of how aggressively questionable billing can affect cash flow. That number should be interpreted carefully because enforcement totals can vary depending on time period, methodology, and whether they reflect announced suspensions, investigations, or related administrative actions. Even so, the message to owners is obvious: buyers know the downside of inheriting a problem file, and they are underwriting accordingly.

What will buyers scrutinize most closely?

Enrollment history: prior revalidations, adverse actions, gaps, ownership changes, branch history, and whether anything in the file could trigger deeper CMS review

Billing patterns: outlier utilization, diagnosis mix, visit intensity, abrupt revenue spikes, questionable recertification patterns, and inconsistencies between clinical records and claims

Compliance infrastructure: internal audits, hotline processes, training logs, survey history, corrective actions, and evidence that issues were addressed

Ownership changes: whether prior transactions were properly disclosed and whether any structure could create CIMO-related questions

State and federal alignment: whether licensure, Medicare enrollment data, and operating footprint all match up cleanly

A buyer today is not just reading your P and L. They are looking for anything that could trigger a holdback, retrade, delayed close, or in the worst case a CMS referral or broader regulatory escalation. If claims look aggressive, if documentation is inconsistent, or if enrollment history raises questions, the value premium attached to scarcity can disappear fast.

This is why operators should stop thinking about diligence as a closing formality. In 2026, diligence is part valuation, part risk triage, and part survivability test.

Three Moves to Make Right Now

If you are an operator navigating the current freeze, here are three immediate priorities to maximize valuation and reduce underwriting risk.

1. Audit Your Billing Records

Start with the last 24 months, and if your agency has had leadership, coding, or census volatility, extend that review to 36 months. Look specifically for:

Claims that were adjusted, reopened, denied, or paid late

Documentation mismatches between clinician notes, OASIS or hospice documentation, and billed services

High-utilization episodes, unusual recertification patterns, or revenue spikes that are hard to explain

Missing physician signatures, late orders, unsupported eligibility narratives, or weak face-to-face documentation where applicable

Branch-level inconsistencies if your operations span more than one service area

Your goal is to assemble a file that is buyer-ready. That means clear support for billed services, a record of internal review, and documented remediation where issues were found. If a buyer samples 30 to 50 charts, you want those charts to tell a clean story without last-minute scrambling.

2. Review Your Payer Mix

A lot of owners still talk about revenue as if all reimbursement is equal. Buyers do not. They want to understand how exposed the agency is to a single payment model, a handful of referral sources, or a margin profile that could change quickly.

Break down your revenue into:

Medicare Fee For Service

Medicare Advantage

Medicaid, where relevant

Commercial or other payer categories

For home health, the mix between Medicare FFS and Medicare Advantage matters because it affects margin predictability, authorization burden, and rate pressure. For hospice, payer mix may look different, but the same balance question applies. A book that is too dependent on one channel may feel less durable under underwriting.

Balanced does not mean perfect symmetry. It means the buyer can see resilience. If Medicare FFS is strong but MA is underdeveloped, that may be fixable. If MA is growing but contracts are weak or denials are elevated, that needs explanation. Build a one-page payer summary showing percentages, trends over the last 12 months, and any major contract or referral concentration. That one page can save weeks of back-and-forth during diligence.

3. Benchmark Your EBITDA

Do not rely on old market talk. Current valuation depends on size, geography, payer profile, compliance cleanliness, management depth, and whether your agency looks like a stable platform or a risk-heavy add-on.

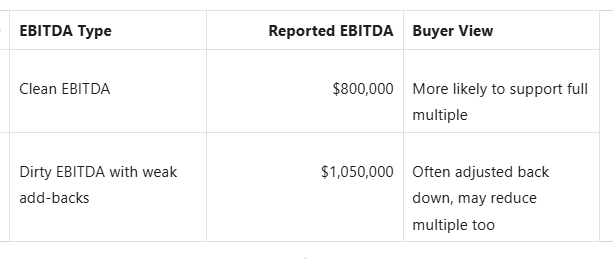

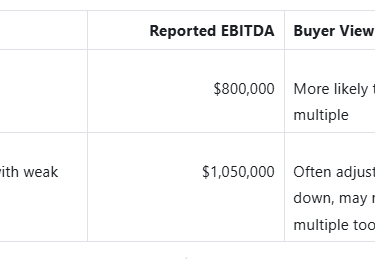

Start by calculating real EBITDA, not owner-adjusted wishful thinking. Buyers will separate:

Clean EBITDA: recurring earnings supported by financial statements, normal staffing, realistic compensation, and documented add-backs

Dirty EBITDA: earnings inflated by temporary understaffing, unsupported add-backs, missing expenses, aggressive revenue recognition, or one-time assumptions that are not credible

A simple example:

Then benchmark against current market ranges. In a constrained market, you may hear wide multiple ranges. That variance exists because different sources track different deal sizes, structures, geographies, and payer mixes. A small owner-dependent agency may trade at one level while a cleaner, manager-run agency with reliable margins trades materially higher. What matters is not the rumor. It is where your agency lands after buyer underwriting.

So what should you do now?

Before you decide whether to hold, grow, or explore a sale, focus on the operator priorities that protect value:

Clean up the last 24 to 36 months of billing and clinical support before a buyer asks for it

Build a simple payer mix dashboard so you can explain revenue stability clearly

Recast EBITDA conservatively and document every legitimate add-back

Reduce key-person dependence by naming operational backups and documenting decision rights

Partnering with Senate Healthcare LLC

At Senate Healthcare LLC, we are not brokers or advisors. We are strategic buyers actively evaluating home health or hospice acquisitions and partnership opportunities.

During a moratorium, our acquisition process becomes even more disciplined because the asset we are evaluating is not just current cash flow. It is also the durability of the provider number, the strength of compliance systems, the quality of leadership transition, and the likelihood of a smooth post-close operating path. That means our review typically centers on four practical areas:

Initial fit review: geography, service mix, size, payer composition, and whether the agency aligns with our acquisition criteria

Confidential operating review: high-level financials, census profile, ownership structure, and major compliance or survey considerations

Focused diligence: billing integrity, enrollment history, management depth, and transition readiness during the current moratorium environment

Transaction discussion: structure, continuity planning, and how to reduce disruption for staff, patients, and referral relationships

Why is Senate well-positioned as a buyer in this environment? Because the market now rewards disciplined acquirers who understand both operations and underwriting risk. We approach home health or hospice opportunities with a practical lens on compliance, continuity of care, and long-term portfolio fit. Owners do not need a perfect story on day one to talk with us. If your agency has strengths but also needs cleanup in certain areas, we can still evaluate whether there is a workable path forward.

For owners facing burnout, succession uncertainty, or concern that waiting may invite more regulatory pressure, this matters. A moratorium can create a window where scarcity improves demand for quality agencies, but that window also comes with heavier scrutiny. We aim to have direct owner-to-buyer conversations that are confidential, realistic, and centered on what protects value.

Ready to discuss the value of your agency?

Contact Senate Healthcare LLC today to explore a partnership or sale.

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED