Home Health Valuation Secrets Revealed: What Your Agency Is Really Worth in 2026

How much of your agency's valuation is real, and how much disappears once buyer diligence starts? This updated guide walks through 2026 EBITDA multiples, the impact of tighter add-back scrutiny, and the operational issues that can create a million-dollar spread in value. You will also see how Senate Healthcare evaluates acquisitions, what buyers want in 2026, and why Medicare Advantage now plays a bigger role in underwriting. If you are a home health or hospice owner thinking about sale timing, this is the practical valuation breakdown to read first.

6/29/202611 min read

Understanding the true market value of your home health or hospice agency is the first step toward a successful exit or strategic partnership. This guide breaks down current 2026 valuation benchmarks and the specific metrics that professional buyers use to determine your agency's price tag.

Here is the hook most owners care about: if two agencies each produce about $700,000 of EBITDA, one can trade around 6.5x and the other can get pushed closer to 4.0x once buyer diligence finds weak documentation, thin management depth, and aggressive add-backs. That spread is roughly $1.75 million in value, which is exactly why exit readiness, underwriting quality, and clean financials matter so much in 2026.

Quick-Scan Summary

Who this is for:

Owner-operators of home health or hospice agencies with $2M to $10M in annual revenue.

Founders looking to understand how buyers like Senate Healthcare evaluate their business.

Owners considering a sale within the next twelve to twenty four months.

Key takeaways:

Valuations in 2026 are heavily influenced by clinical quality scores, payer diversification, and buyer underwriting scrutiny.

Average EBITDA multiples for mid-sized agencies currently range from 4.0x to 7.5x, with stronger outcomes for cleaner operations and lower-risk earnings.

Add-backs are getting tighter, with market tolerance often closer to 12 to 15 percent instead of the roughly 20 percent some owners expected in prior years.

Operational independence from the owner is a major driver of premium pricing.

Senate Healthcare is actively looking to acquire agencies that meet these quality benchmarks.

The 2026 Market Context: Why Valuations Are Shifting

The landscape for home health or hospice M&A has evolved significantly as we move through the middle of 2026. While the post-pandemic boom has stabilized, the demand for high quality home-based care remains at an all-time high. Recent data from the Hendon Partners Q2 2026 Report shows a sharp rebound in transaction volume, with roughly ninety five to one hundred ten tracked transactions and disclosed deal value above $4.2 billion in the quarter.

Buyers are no longer just looking for census numbers. They are looking for stability, documentation quality, scalable operations, and risk-adjusted earnings. With interest rates leveling off and more capital coming back into the sector, the focus has shifted toward operational efficiency and clinical excellence. As a buyer, Senate Healthcare prioritizes agencies that have successfully navigated the transition to newer payment models and have maintained a strong workforce in a competitive labor market.

The underwriting gap is also widening. Research from FOCUS Bankers' 2026 EBITDA multiples report and the Stoneridge Partners 2026 outlook points to the same reality: quality assets are still getting strong attention, but average agencies are seeing more scrutiny and less forgiveness. That matters for owner-operators because even a decent agency can lose multiple turns of value if buyers find referral concentration, reimbursement pressure, weak compliance reporting, or owner dependence during diligence.

Common Owner Pain Points and Valuation Haircuts

Many owners reach out to us when they feel the weight of succession risk or burnout. If you are the primary person holding your agency together, your business might suffer from key-person dependence. This is one of the most common reasons for a valuation haircut: a reduction in the expected sale price.

If the business cannot function for thirty days without your direct involvement, a buyer sees higher risk. Other common pain points include:

Succession Uncertainty: Not having a clear second-in-command to take over operations.

Medicare Advantage Pressure: Low-margin contracts that eat into your bottom line.

Underwriting Scrutiny: Buyers today are performing deeper audits on clinical documentation, coding, compliance, and the reliability of adjusted EBITDA.

Referral Concentration: If too much volume comes from one hospital system, physician group, or discharge channel, a buyer will treat the revenue as more fragile.

Messy Add-Backs: According to Vallexa Advisors' 2026 valuation analysis, buyers are less willing to accept loose normalization adjustments and are tightening accepted add-backs closer to 12 to 15 percent versus the roughly 20 percent some owners may have expected.

Management Thinness: A business with no real bench under the founder often gets underwritten as a riskier transition.

A simple way to think about it is this: buyers are paying for future cash flow they believe will hold up after closing. Anything that makes that cash flow look less durable can lower your multiple, reduce your sale price, or change the structure of the deal.

The Math: How We Value Your Agency

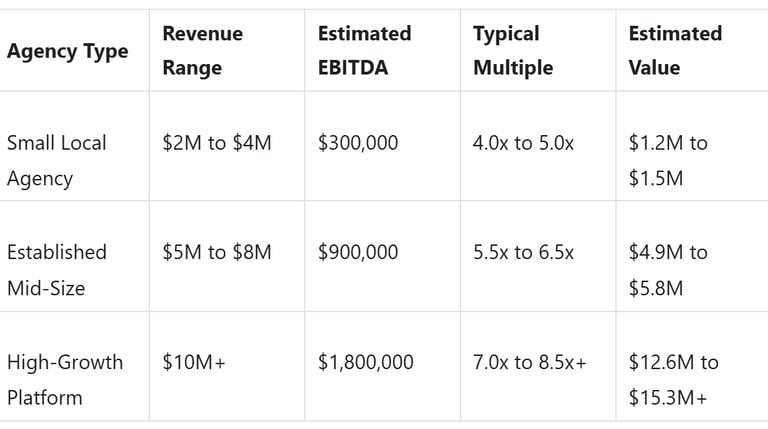

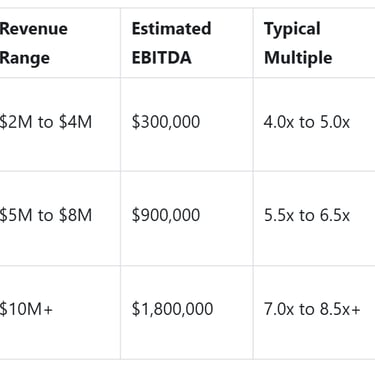

Valuation is not just a guess. It is based on a multiple of your Earnings Before Interest, Taxes, Depreciation, and Amortization, also known as EBITDA. According to the FOCUS Bankers 2026 EBITDA Multiples report, agencies in the $2M to $10M revenue range are seeing a clear spread in multiples based on their size, payer mix, compliance posture, and clinical performance.

Below is a simple breakdown of how these multiples translate into real dollars for your home health or hospice agency.

As the buyer, Senate Healthcare looks at these ranges as a starting point. We also consider add-backs, which are expenses that won't continue after the sale, such as your personal travel or one-time legal fees. But in 2026, accepted add-backs are under more pressure. Per Vallexa Advisors' 2026 valuation article, buyers are tightening normalization and often pushing accepted add-backs into the 12 to 15 percent range rather than letting sellers stretch toward roughly 20 percent.

That tightening can materially change value. If an owner thought they had $800,000 of adjusted EBITDA but only $700,000 is truly supportable after diligence, a one-turn change in multiple can quickly turn into a seven-figure reduction in enterprise value.

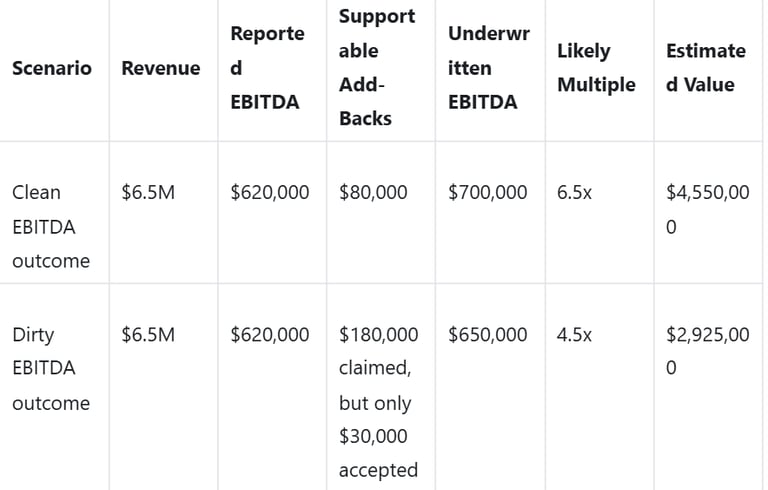

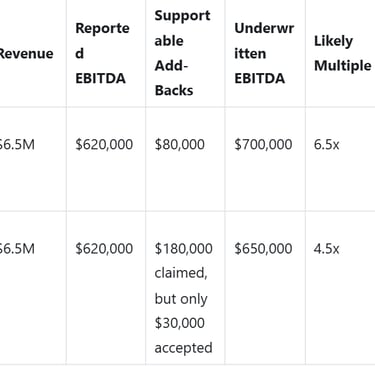

Clean vs. Dirty EBITDA: A Real 2026 Valuation Spread

The difference between a clean story and a messy one is where many owners either protect value or lose it. Here is a practical example for a mid-sized agency in Senate Healthcare's target range.

That is a difference of $1,625,000 in value.

Why does that happen? Usually because the "dirty" version comes with some combination of undocumented add-backs, weak collections, owner-heavy operations, patchy documentation, payer concentration, or compliance questions. The business may still be real and still be sellable, but the buyer underwrites it more conservatively.

For owners thinking about sale price, this is the key lesson: valuation upside does not come only from growing revenue. It often comes from making your EBITDA more believable and your operations easier to transfer.

Why Quality of Earnings (QoE) Matters Now More Than Ever

In 2026, the Stoneridge Partners 2026 outlook highlights that a clean Quality of Earnings review can be the difference between a deal closing smoothly and a deal getting repriced. Buyers like us are looking for sustainable cash flow. If your revenue is tied 90 percent to a single referral source or a low-paying Medicare Advantage contract, the risk profile increases.

We prefer to see a healthy mix of payers and a diversified referral base. This reduces the risk that a single change in the market will sink the business after we acquire it.

What Buyers Are Looking for in 2026

Based on the 2026 research from Hendon Partners, FOCUS Bankers, Stoneridge Partners, and Vallexa Advisors, buyers are rewarding agencies that can prove earnings durability, clinical consistency, and transferability. In plain English, here is what gets attention in today's market:

Supportable EBITDA: Not just a higher number, but a number that survives diligence.

Disciplined Add-Backs: Clear documentation for every adjustment, with fewer aggressive assumptions.

Diversified Payer Mix: Traditional Medicare stability, manageable Medicare Advantage exposure, and no single contract that can crush margin.

Referral Diversity: No overdependence on one hospital, one physician group, or one community relationship.

Management Depth: A clinical and operational team that can run the business without the founder in every decision.

Documentation Integrity: Eligibility, coding, face-to-face records, orders, and billing support that hold up under review.

Quality and Compliance Signals: Clean survey history, strong outcomes, and no unresolved audit issues.

Staffing Stability: Better retention, controllable overtime, and less chaos in scheduling.

Clear Growth Story: Not fantasy growth, but realistic branch density, recruiting capacity, and margin improvement opportunities.

For a home health or hospice owner in the $2M to $10M revenue range, these are not abstract banker talking points. These are the operational details that can influence multiple, structure, and buyer confidence.

How Senate Healthcare Evaluates Agencies in Acquisition Due Diligence

As the buyer, Senate Healthcare does not evaluate an agency based on revenue alone. We look at whether the business can continue producing quality care and reliable earnings after transition. That means our acquisition due diligence typically centers on a few practical questions:

Are the earnings real? We review P&Ls, general ledger detail, owner compensation, one-time costs, and whether claimed add-backs are actually supportable.

Can the business run without the owner? We assess leadership depth, scheduling control, intake flow, clinical oversight, and whether there is a credible second layer of management.

Is payer risk manageable? We examine traditional Medicare exposure, Medicare Advantage penetration, contract economics, denials, and margin by payer category.

Are referrals durable? We want to see diversified referral relationships, not a business held together by one or two sources.

Is compliance likely to hold up? We look at documentation quality, survey history, billing discipline, and any signs of audit exposure or operational shortcuts.

Can we underwrite growth responsibly? We evaluate staffing capacity, market density, branch scalability, and whether current margins are sustainable.

This is why owner preparation matters so much. Senate Healthcare may still evaluate an agency that is not perfect today, but the more risk we need to absorb, the more pressure that creates on multiple, structure, or both.

An Anonymized Owner Vignette

One owner we will call "Maria" ran a home health agency with about $5.8 million in revenue. On paper, the business looked strong. Census was stable, the local reputation was solid, and adjusted EBITDA appeared to be just over $750,000.

But when a buyer started digging in, three issues surfaced. First, too much of the business still ran through Maria personally. Second, almost one third of referrals came from a narrow channel. Third, several add-backs were more optimistic than supportable. The result was not that the business became unsellable. The result was that the buyer underwrote less EBITDA and assigned a lower multiple because transition risk was higher.

The good news is that this kind of story can improve. After cleaning up the financial presentation, strengthening operational delegation, and reducing concentration, the agency became much easier to underwrite. That is the reality many owners need to hear: you do not need to be perfect to have a path forward, but the buyer's view of risk will directly affect value.

Plain-Language Glossary

Adjusted EBITDA: EBITDA after removing unusual, nonrecurring, or owner-specific items that a buyer believes will not continue.

Add-back: An expense added back to profit because it is not expected to continue after the sale, but only if it is real, documented, and defensible.

Average Daily Census: The average number of patients on service each day. Buyers use it to assess scale and stability.

Buyer Underwriting: The process a buyer uses to decide what cash flow is real, what risks exist, and what price makes sense.

Cash Flow Durability: How likely earnings are to continue after closing.

Compliance Risk: The chance that billing, documentation, or regulatory issues could create repayment, audit, or licensing problems.

EBITDA: A measure of a company's overall financial performance, often used as a proxy for cash flow.

Enterprise Value: The total value of the business before debt, cash, and certain deal-specific adjustments.

Haircut: A slang term for a reduction in the offered price due to discovered risks during due diligence.

Key-Person Dependence: When the owner is so central to the business that performance may drop after the owner leaves.

Letter of Intent: A nonbinding document that outlines the basic purchase terms before full diligence and final agreements.

Medicare Advantage: Medicare coverage administered by private plans, often with different rates, authorization rules, and margin implications than traditional Medicare.

Multiple: The number used to multiply your EBITDA to find the total business value.

Platform vs. Add-on: A platform is a larger agency used as a base for growth, while an add-on is a smaller agency integrated into an existing platform.

Quality of Earnings: A deeper financial review that tests whether reported earnings are accurate, sustainable, and transferable.

Referral Concentration: Too much business tied to too few referral sources.

Retrade: When a buyer lowers price or changes terms after finding new issues in diligence.

Working Capital: The short-term operating assets and liabilities needed to keep the business running after closing.

The Role of Medicare Advantage in Your Valuation

It is no secret that Medicare Advantage is taking a larger share of the market, and in 2026 buyers are paying closer attention to what that means for actual margin. The FOCUS Bankers 2026 report notes that payer mix is one of the clearest drivers of multiple outcomes, with heavy Medicare Advantage concentration often compressing margins and reducing valuations. The Stoneridge Partners 2026 outlook makes a similar point: fee-for-service Medicare still acts as the baseline for many buyers, while Medicare Advantage can either help or hurt value depending on contract quality and execution discipline.

That does not mean Medicare Advantage is automatically bad. It means buyers will ask harder questions:

What percentage of revenue is tied to Medicare Advantage?

Are authorizations slowing care delivery or increasing administrative cost?

Are gross margins by payer category clearly tracked?

Can the agency manage visit utilization without eroding quality?

Are denials, recerts, and collections materially worse under certain plans?

For some agencies, strong Medicare Advantage operations can be a plus. If you have disciplined intake, tight authorization management, and acceptable margins by contract, that can signal operational maturity. But if Medicare Advantage is growing and the agency cannot show profitability by payer, the buyer may underwrite lower cash flow or apply a lower multiple.

The practical takeaway is simple. In 2026, Medicare Advantage is no longer a side note in valuation. It is part of underwriting. For both home health and hospice owners, payer mix needs to be explained in a way that shows earnings are durable and not just temporarily propped up by volume.

So what should you do now?

If you are thinking about the future of your home health or hospice agency, here are the steps you should take today:

Audit Your Financials: Ensure your books are clean, separate from personal expenses, and backed by support for every add-back.

Build Your Bench: Empower a clinical manager or administrator to handle daily operations without you.

Review Your Payer Mix: Look for ways to diversify beyond a single major contract and understand your real margins by payer.

Reduce Concentration Risk: Strengthen your referral base so no single source can materially shake the business.

Know Your Number: Understand what your agency is worth today so you can plan for tomorrow.

Partner with Senate Healthcare

Senate Healthcare is not a broker or an advisor. We are the buyer. We are an acquiring entity looking to grow our portfolio of high quality home health or hospice agencies, and we evaluate opportunities through the lens of long-term care quality, sustainable operations, and realistic underwriting. We understand the blood, sweat, and tears you have poured into your business.

If you are exploring a sale, succession plan, or partnership with an acquirer, our goal is to help you reduce transition risk, improve exit readiness, and have a practical conversation about what your agency may look like in a real buyer process. Even if your agency is not perfectly positioned today, we are open to evaluating situations where the fundamentals are sound and the path to stronger performance is clear.

If you are ready to explore a sale or want to see how your agency fits into our acquisition strategy, visit us at www.senatehealthcare.com to start a confidential conversation.

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED