7 Mistakes You’re Making with the 36-Month Rule (And How They Kill Your Exit)

This article breaks down the high-stakes world of the 36-month rule and the 2026 CMS moratorium for home health or hospice owners. We identify seven common mistakes that can lead to frozen billing privileges and massive valuation haircuts during a sale. Learn how to leverage exceptions and structure your business to ensure a successful and profitable exit.

5/21/20266 min read

This guide examines how the 36-month rule and the 2026 CMS moratorium impact home health or hospice agency valuations and sales. Understanding these regulatory hurdles is essential for owners looking to maximize their exit price and avoid deal-breaking delays in the current market.

Quick-Scan Summary

Who this is for:

Owners of home health or hospice agencies with $2M to $10M in annual revenue.

Operators planning a sale or partnership within the next 12 to 24 months.

Entrepreneurs who have recently acquired an agency or expanded their footprint.

Key takeaways:

The 36-month rule (42 CFR § 424.550(b)) can trigger a total loss of billing privileges during a sale if the agency is less than three years old.

The 2026 CMS nationwide moratorium makes asset sales almost impossible for many agencies because it blocks new Medicare enrollments.

Strategic use of the "Two-Year Cost Report" exception and indirect ownership structures can save a deal from collapse.

Agencies that fall into the 36-month trap face significant valuation "haircuts" due to buyer risk and potential billing gaps.

The 2026 Regulatory Landscape: A New Reality for Owners

As of May 2026, the landscape for home health or hospice M&A has shifted dramatically. CMS has implemented a nationwide enrollment moratorium for new home health agencies and hospices. This is not just a pause for new startups; it directly affects existing agencies trying to sell. Under the 36-month rule, if a transaction is classified as a Change in Majority Ownership (CIMO), the buyer is often treated as a new enrollee. During this moratorium, those new enrollments are being denied.

This means if your agency is "young" or has recently changed hands, you might be stuck in an illiquid position. At Senate Healthcare, we are evaluating acquisitions specifically through the lens of these new rules to ensure our partners can transition their businesses without facing a catastrophic billing freeze.

1. Thinking the Rule Only Applies to Home Health

For years, the 36-month rule was a problem primarily for home health agencies. However, the CY 2024 Home Health PPS Final Rule officially extended these same restrictions to hospices. If you own a hospice and assume you can flip the business within two years of opening or buying it, you are mistaken. The clock starts the moment you receive your initial Medicare enrollment or the date of your last CIMO.

The Fix: Treat your hospice agency with the same regulatory caution as a home health agency. Ensure your compliance team tracks the exact date of your initial enrollment or last majority sale to know exactly when your 36-month window closes.

2. Planning an Asset Sale During the 2026 Moratorium

In a typical asset sale, the buyer acquires the assets but usually applies for a new Medicare Provider Number (CCN). Under the current moratorium, CMS is denying these new enrollments. If you insist on an asset deal to ring-fence historical liabilities, you may find that the buyer cannot actually bill Medicare once the deal closes. This creates an immediate "no-sale" environment for asset-heavy structures.

The Fix: Pivot toward equity or stock transactions. By selling the entity itself, you preserve the existing CCN and billing privileges. While this requires more rigorous due diligence regarding historical liabilities, it is often the only viable path forward during a moratorium.

3. Miscalculating the "Two-Year Cost Report" Exception

There is a common myth that you must wait a full 36 months to sell. In reality, 42 CFR § 424.550(b)(2) provides an escape hatch. If the home health or hospice agency has submitted two consecutive years of full cost reports since its initial enrollment or last majority change, the rule does not apply. However, many owners fail to realize that "low-utilization" or "no-utilization" cost reports do not count toward this exception.

The Fix: Audit your cost report history immediately. Confirm that you have two back-to-back years of "full" reports. If you had a period of low census where you filed a low-utilization report, your 36-month clock likely did not accelerate, and you may be stuck waiting the full three years.

4. Ignoring the Benefits of Indirect Ownership

The 36-month rule specifically targets "direct" ownership changes of more than 50 percent. Many owners own their agency directly as individuals or through a simple LLC. When it comes time to sell, this direct transfer triggers the rule. Strategic operators often use a holding company (HoldCo) structure where the HoldCo owns the agency.

The Fix: While you cannot usually change your structure right before a sale to dodge the rule, long-term planning involves holding your agency through a parent entity. Changes at the parent or grandparent level are often treated as a Change of Information (COI) rather than a CIMO, which can bypass the 36-month restriction entirely.

5. Overlooking the "Cumulative Effect" of Small Sales

You might think that selling 20 percent of your agency this year and another 35 percent next year keeps you safe because neither is "majority" ownership. This is incorrect. CMS looks at the cumulative effect of transactions within a rolling 36-month window. If the total percentage of direct ownership transferred exceeds 50 percent in that timeframe, you have triggered a CIMO.

The Fix: Maintain a strict "cap table" and transaction log. Before selling even a minority stake to a partner or key employee, calculate how that impacts your ability to sell the remaining portion of the company within the next three years.

6. Failing to Identify "Seasoned" vs. "Young" Status

In the 2026 market, there is a massive valuation gap between "seasoned" agencies (those outside the 36-month window) and "young" agencies. Seasoned agencies are scarce and carry a premium because they can be acquired without the risk of a billing freeze. Young agencies are often viewed as "distressed" or "high-risk" simply because of their age, regardless of their clinical quality.

The Fix: If you are within the 36-month window, recognize that you are in a weak negotiating position for a traditional sale. You should focus on operational excellence to prove your value or look for a strategic buyer like Senate Healthcare that understands how to navigate these regulatory complexities.

7. Underestimating Buyer Underwriting Scrutiny

Because the moratorium forces buyers into equity deals, they are now inheriting all your past mistakes. Every billing error, HR dispute, and compliance lapse from the last three years becomes the buyer’s problem. If your documentation is messy, buyers will either walk away or demand massive holdbacks that can reach 20 to 30 percent of the total sale price.

The Fix: Conduct a "sell-side" audit at least one year before you plan to exit. Clean up your charts, resolve any outstanding ADRs (Additional Documentation Requests), and ensure your corporate minutes are up to date. Reducing the buyer's risk profile is the fastest way to increase your final payout.

Valuation Math: The Cost of the 36-Month Rule

To illustrate the impact, let's look at two hypothetical hospice agencies, both generating $1M in EBITDA.

Agency A (Seasoned):

In operation for 5 years.

No ownership changes in 36 months.

Valuation Multiple: 6.5x EBITDA.

Sale Price: $6.5 Million.

Exit Environment: High competition among buyers; smooth transition.

Agency B (Within 36-Month Window):

In operation for 2 years.

One low-utilization cost report filed.

Valuation Multiple: 4.5x EBITDA (due to "illiquidity discount" and moratorium risk).

Sale Price: $4.5 Million.

Exit Environment: Limited buyers; 20% escrow holdback for 24 months.

In this scenario, failing to manage the 36-month rule costs the owner $2 Million in total valuation and significantly worse deal terms.

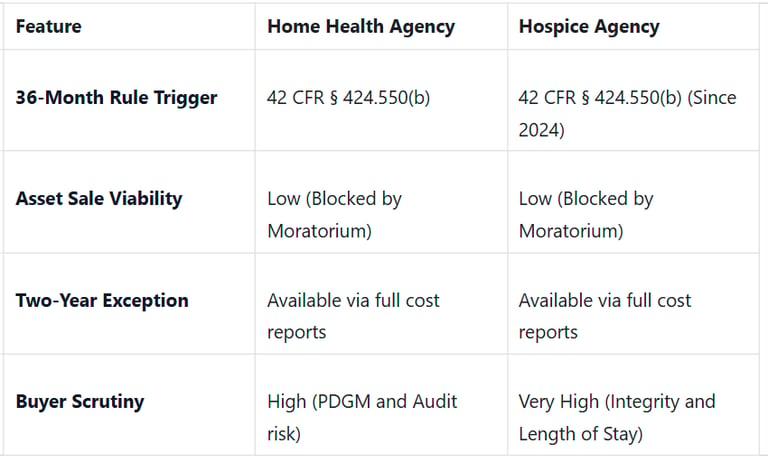

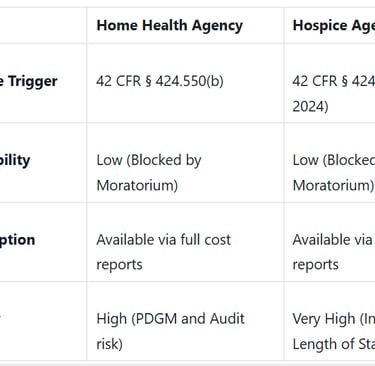

Home Health vs. Hospice: A Comparison of Exit Readiness

Plain-Language Glossary

CIMO (Change in Majority Ownership): When more than 50 percent of the direct ownership of an agency changes hands.

CCN (CMS Certification Number): Your agency's "Social Security Number" for Medicare billing.

Moratorium: A government-mandated freeze on new business activities, in this case, new Medicare enrollments.

EBITDA: A measure of your company's profitability used to determine its value (Earnings Before Interest, Taxes, Depreciation, and Amortization).

Haircut: A reduction in the expected sale price or valuation of a business.

So what should you do now?

Check your dates: Find your original Medicare tie-in notice or your last CIMO closing documents to confirm exactly where you stand on the 36-month clock.

Verify your cost reports: Ask your accountant if your last two reports were "full" or "low-utilization" to see if you qualify for an early exit exception.

Evaluate your structure: If you are planning to grow or acquire other agencies, talk to legal counsel about using a holding company to simplify future transitions.

Assess your risk: Use the valuation examples above to see if waiting another year could net you a significantly higher multiple.

Senate Healthcare is currently seeking to partner with and acquire home health or hospice agencies that are navigating these complex regulatory waters. We focus on operational excellence and long-term sustainability. If you are an owner looking to reduce your risk or explore a sale, contact us to discuss how we can help you maximize the value of your legacy.

Unlock Your 30-Minute Agency Succession Review

Maybe you're ready to expand your reach, or perhaps it's time to consider your legacy and the future of your business. Either way, it all begins with a conversation. Schedule a confidential, no-obligation call to explore what the future might hold for you and your business.

Complete the form, and we'll reach out for a chat...

© 2025 SENATE HEALTHCARE LLC.

ALL RIGHTS RESERVED